Market Mayhem · Episode 05 · October 1929 · USA

Black Tuesday: The Day America Stopped Believing

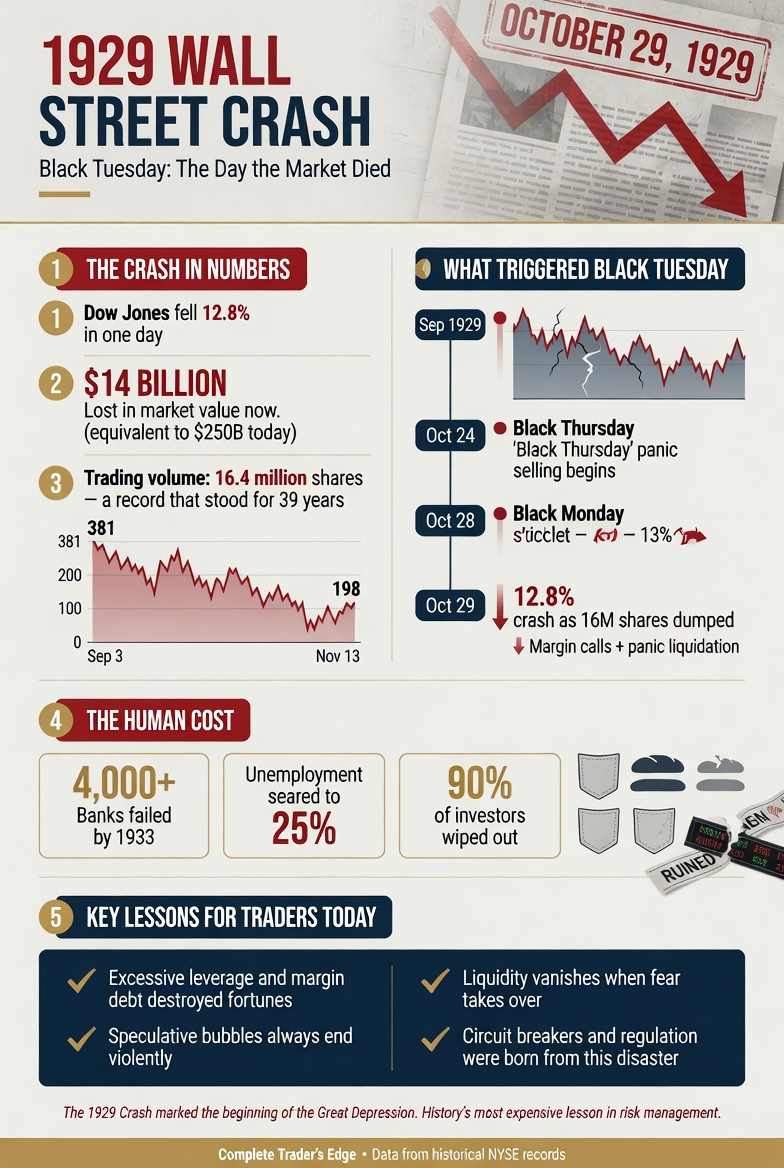

$14 billion. One day. The crash that started the Great Depression.

Jesse Livermore shorted it perfectly and made $100 million. Then lost it all. Then never recovered.

Also available on Apple Podcasts · Amazon Music · iHeart Radio

📄 Free Download · Episode Research Sheet

Black Tuesday Research Sheet (PDF)

The full timeline, key numbers, the Mind, Method, Money lessons, and further reading from this episode. Free, no email required.

On the morning of October 29th, 1929, the opening bell of the New York Stock Exchange rang at ten o’clock. Before the echo faded, the selling began.

Not orderly selling. Not professional portfolio adjustments. Raw panic — moving through the trading floor like fire through a building with no exits. The ticker tape, the mechanical printer that transmitted stock prices to brokerage offices across America, was already running hours behind. There were so many sell orders flooding in simultaneously that the system built to record them could not keep pace with the destruction.

By the closing bell: fourteen billion dollars in market value had simply ceased to exist.

Outside on Broad Street, a crowd stood in silence. Not running. Not shouting. Just standing. Staring at the building. As if watching from outside might tell them something about the ruin being conducted within.

The crash of 1929 did not just end the Roaring Twenties. It began a decade of suffering that reshaped American society permanently — and it remains the definitive lesson in what leverage does when markets reverse.

The Crisis at a Glance

| Data Point | Detail |

|---|---|

| Event | Wall Street Crash of 1929 — the trigger event of the Great Depression |

| Black Thursday | October 24, 1929 — first major panic; 11% single-day drop; temporary banker intervention |

| Black Monday | October 28, 1929 — Dow falls 12.8% in a single day |

| Black Tuesday | October 29, 1929 — $14 billion lost in one day; ticker tape hours behind |

| Dow Peak (Sep 1929) | 381 points |

| Dow Bottom (Jul 1932) | 41 points — an 89% decline over 3 years |

| Recovery Time | 25 years — 1929 highs not recovered until 1954 |

| Margin Lending at Peak | Over $8 billion in brokers’ loans; standard leverage ratio 10:1 (10% deposit, 90% borrowed) |

| Jesse Livermore’s Short Profit | Estimated $100 million (~$1.5 billion today) — the greatest single trade in American history at that time |

| Livermore’s Fate | Declared bankruptcy 1934. Died by suicide November 28, 1940. |

| Regulatory Response | Securities Exchange Act 1934 (created the SEC); Glass-Steagall Act; federal deposit insurance; tighter margin requirements |

| M·M·M Lesson | Money — leverage destroyed millions. Mind — certainty of permanent prosperity. Method — Livermore: right call, unsustainable process. |

The Roaring Twenties: A Borrowed Boom

America in the nineteen-twenties was extraordinary. The war was over, the economy was genuinely growing, and a cascade of new technologies — the automobile, the radio, the telephone — was creating industries, jobs, and consumers in a self-reinforcing cycle of prosperity.

The Dow Jones Industrial Average climbed from roughly 100 in 1921 to 381 by September 1929. A near four-fold increase in eight years. And critically — not entirely without foundation. American corporate profits had genuinely grown. The productivity gains were real. The stock market’s rise reflected, at least in its earlier stages, something that had actually happened in the economy.

Then margin lending changed everything.

Brokers began offering investors the ability to buy stocks with borrowed money — putting up ten percent of their own capital, borrowing ninety percent. If you had $100, you could control $1,000 of stock. A ten percent rise doubled your money. A ten percent fall wiped it out entirely — plus the loan.

This was not unusual or fringe. It was the dominant mode of stock market participation in the late 1920s. At peak, brokers’ loans totalled over $8 billion. Hundreds of thousands of Americans — factory workers, schoolteachers, secretaries — had borrowed their way into the market. And the market had rewarded every one of them, every time, until the morning it didn’t.

John J. Raskob of General Motors published an article in August 1929 titled “Everybody Ought to Be Rich” — arguing that ordinary Americans who invested modestly in stocks would retire wealthy. It was read by millions. It ran three months before the crash.

Jesse Livermore: The Man Who Saw It Coming

Jesse Livermore was 52 years old in 1929. A veteran of the 1907 panic and the 1920 crash, a man who had made and lost multiple fortunes and whose accumulated experience gave him something the newly minted market enthusiasts entirely lacked: perspective.

He saw the margin loans. He saw the valuations — Radio Corporation of America trading at over 500 times earnings it didn’t yet have. He watched ordinary people borrowing money they didn’t have to buy assets they didn’t understand at prices that couldn’t be justified by any analysis of underlying business value.

He started building short positions. Quietly, across multiple accounts, spread across multiple brokers so no single party could see the full scope of what he was doing. He was betting — enormous sums — that the greatest bull market in American history was about to reverse.

His wife begged him to stop. His friends told him he was wrong. The market kept rising. His short positions lost money as it went higher. The social pressure of being the man betting against American prosperity was immense.

He held. He did not close. He waited.

In October 1929, the market agreed with him. And when it did, it agreed completely and all at once.

Four Days That Changed America

Black Thursday, October 24: The crack appears. Eleven percent intraday decline. Ticker tape two hours behind. Bankers make a dramatic public appearance on the floor, buying steel shares at above-market prices to signal confidence. It works — for three days.

Black Monday, October 28: The selling resumes. No bankers appear. Margin calls go out automatically. Investors who cannot meet them have positions liquidated at whatever price the market will bear. The Dow falls 12.8%.

Black Tuesday, October 29: The worst day in American stock market history. Sell orders accumulated since the previous close hit simultaneously at the opening bell. The ticker falls so far behind that prices printed in the afternoon are from hours earlier. Men on the floor describe a sound unlike anything they had heard before. $14 billion. Gone. In one day.

The selling continued for weeks. The Dow lost nearly 50% by mid-November. By its final bottom in July 1932: 89% below the September 1929 peak. Recovery to those highs took 25 years.

The margin calls that destroyed investors also destroyed the banks that had made the loans. Bank failures destroyed the deposits of people who had never owned a single share. What began as a stock market crash became a banking crisis became an economic collapse. The Great Depression — ten years of mass unemployment, farm failures, breadlines, and human suffering — was built on the rubble of October 1929.

Livermore’s Tragedy

Jesse Livermore made approximately $100 million. He received death threats. He needed bodyguards. He gave large sums away. He invested in new ventures. He continued trading.

By 1934, he was bankrupt. The hundred million was gone and more. His methods, his discipline, his extraordinary pattern recognition — the same capabilities that had identified and capitalised on the greatest crash in American history — were not enough to sustain a lifetime of consistent performance. The psychological weight of being Jesse Livermore, of having seen and done everything, had eroded something beneath the surface.

On November 28, 1940, he walked into the cloak room of the Sherry-Netherland Hotel in New York and took his own life. His note to his wife read, in part: “My life has been a failure.”

The man who made the greatest trade in American history died believing he had failed. There is no clean lesson in that. Only the acknowledgement that genius is not a guarantee, and that the market — and life — requires not one correct call but a lifetime of sustainable process.

What This Means for You as a Trader

💰 MONEY — Leverage Is Not an Amplifier of Returns

It is an amplifier of outcomes. The margin investors of 1929 did not necessarily choose bad businesses. They held them at 10:1 leverage. When the market moved against them, the loans called, the positions liquidated, and the loss was total. At 1% risk per trade, twenty consecutive losses leaves you at 82 cents on the dollar — recoverable. At 10% risk, the same losing streak takes you to 12 cents. The math is merciless. Position sizing is not a preference. It is the variable that determines whether you survive long enough to be right.

🧠 MIND — When Caution Feels Socially Unacceptable

In 1929, the optimism was not baseless in its origins. The economy genuinely had grown. Corporate profits genuinely had risen. But by the late stages, valuations were disconnected from any underlying reality, and cultural certainty had made caution feel not prudent but unpatriotic. When the consensus of a bull market crowd makes being careful feel embarrassing, you are in the late stages of a bubble. The crowd’s certainty is the signal, not the evidence.

📊 METHOD — Being Right Is Not Enough

Livermore was right. Completely, historically right. He identified the bubble, built the correct position, held through enormous pressure, and captured one of the greatest trades in history. And he still ended his life in ruin. Because being right about one trade — even a $100 million trade — is not the same as having a repeatable, sustainable process. Your edge must be a system, not a moment. The genius trade cannot sustain the rest of your trading life. What sustains it is the process that produces consistent, manageable, recoverable results across hundreds of trades, not one spectacular one.

Frequently Asked Questions

What exactly caused the 1929 crash?

The proximate cause was margin calls — the automatic liquidation of leveraged positions when share prices fell below the collateral threshold. But the underlying cause was a valuation bubble built on ten-to-one borrowed money. When prices began declining for any reason, the margin calls created forced selling, which drove prices lower, which triggered more margin calls. The cascade was self-sustaining once it started. The fundamental problem was not investor psychology or any single event — it was the leverage structure that meant a modest price decline became a catastrophic liquidation spiral.

How did Jesse Livermore know the crash was coming?

He didn’t “know” in any supernatural sense. He analysed the market the way he had been doing for thirty years: looking at the overall pattern of prices, the behaviour of leading stocks, the level of margin lending, and the relationship between valuations and underlying business earnings. What he concluded was that the risk-reward of being long was catastrophically unfavourable. He was not certain the crash would happen in October 1929. He was certain that at some point the leverage structure of the market would force a liquidation cascade. He positioned accordingly and held his position through the period when the market disagreed with him.

How long did the Great Depression last?

From the crash in 1929 to the full economic recovery, approximately a decade. US unemployment peaked at nearly 25% in 1933. GDP did not return to 1929 levels until 1939–1940, coinciding with rearmament spending ahead of the Second World War. The Dow Jones Industrial Average did not recover its 1929 peak until 1954 — twenty-five years after the crash. This is the counterargument to the market bromide that “markets always recover eventually.” They do. But “eventually” can mean a generation.

What regulations came out of 1929?

The regulatory response was comprehensive and lasting. The Securities Act of 1933 required companies to disclose material information when issuing securities. The Securities Exchange Act of 1934 created the Securities and Exchange Commission and regulated secondary market trading. The Glass-Steagall Act separated commercial and investment banking. Federal deposit insurance was introduced, preventing bank runs from destroying ordinary depositors. Margin requirements were tightened significantly. Much of the architecture of modern financial regulation was built directly on the lessons of 1929.

Could something like the 1929 crash happen today?

The specific mechanics — ten-to-one margin lending with no circuit breakers, no deposit insurance, no lender of last resort — are different. Modern markets have circuit breakers, regulated margin requirements, central bank backstops, and deposit insurance. But the underlying human dynamics — leverage amplifying both sides of a market move, valuations disconnecting from fundamentals during prolonged bull markets, FOMO driving late-stage buying — are unchanged. The 2000 dot-com crash, the 2008 financial crisis, and the 2022 crypto collapse all share structural DNA with 1929. The specific instrument changes. The pattern does not.

What is the most important risk management lesson from 1929?

Never use leverage that makes a normal market correction into a personal catastrophe. The investors of 1929 were not necessarily wrong about the long-term value of American industry. Many of the companies they held were genuinely good businesses that did recover — eventually. But they held those businesses with borrowed money at ratios that meant a thirty or forty percent market decline wiped out not just their investment but created additional obligations. The discipline: never hold a position where a normal, historically typical market decline forces you out of the trade before your thesis has time to play out.

Continue the Market Mayhem Series

Next: Silver Thursday — Corner the World’s Silver

1980. Two brothers. Sons of the richest man in America. A plan to corner the entire global silver market. And the day the exchange changed the rules to stop them.

⚡ Modern Echo · 2026

1929 was margin loans at 10% down and a market priced for a new era of permanent prosperity. In 2026, the Shiller CAPE is 40 (only ever matched in 2000), the Buffett Indicator is at 219%, and the AI story is doing what “new era” always does. The setup is back.

Read: The Next Market Crash — 5 Scenarios That Could End the Bull Run →

Market Mayhem is a historical education series produced by The Complete Trader’s Edge. All figures are sourced from historical records. Content is for educational purposes only and does not constitute financial or investment advice. Trading involves significant risk of loss.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →