Market Mayhem · Episode 06 · 1980 · USA

Corner the World’s Silver

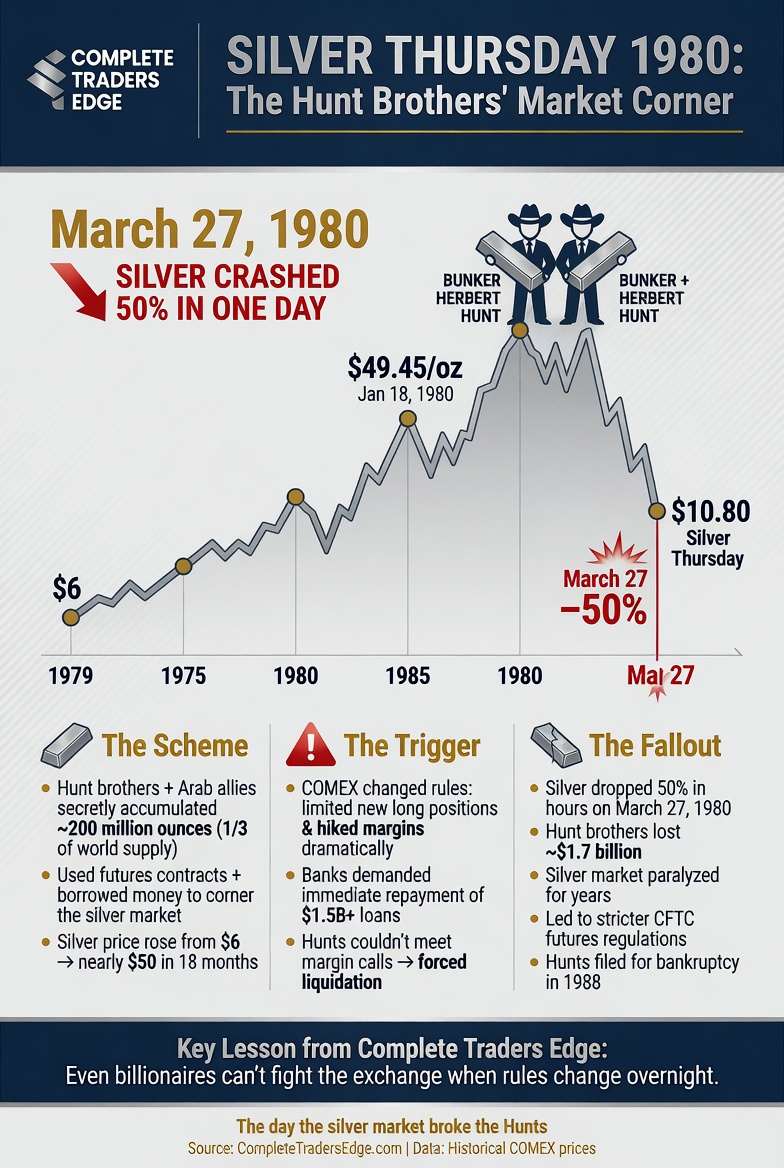

The Hunt Brothers, Silver Thursday, and the Day the Exchange Changed the Rules

Two billionaire brothers accumulated one-third of the world’s privately held silver. Then the exchange banned new buying. And in one day, it was over.

▶ Watch on YouTube🎵 Listen on Spotify

Also available on Apple Podcasts · Amazon Music · iHeart Radio

📄 Free Download · Episode Research Sheet

Silver Thursday Research Sheet (PDF)

The full timeline, key numbers, the Mind, Method, Money lessons, and further reading from this episode. Free, no email required.

In the winter of 1979, two brothers from Texas were doing something that should have been impossible.

Nelson Bunker Hunt and William Herbert Hunt — sons of H.L. Hunt, once estimated to be the wealthiest private individual in the United States — had systematically accumulated an estimated two hundred million troy ounces of silver. Physical bars. Coins. Futures contracts. In a world that produced roughly five hundred million troy ounces from all mines combined in an entire year, two men had quietly taken control of approximately one third of the world’s privately held supply.

Silver had been around six dollars per ounce when they started. By January 1980, it touched fifty dollars and thirty cents — an 800% rise in under three years.

Then the exchange changed the rules. And in a single day, everything the Hunts had built collapsed.

The Crisis at a Glance

| Data Point | Detail |

|---|---|

| Event | Silver Thursday — collapse of the Hunt Brothers’ silver market corner |

| Date | March 27, 1980 |

| Key Figures | Nelson Bunker Hunt and William Herbert Hunt; Saudi partners through IMIC; Paul Volcker (Federal Reserve) |

| Silver (Jan 1979) | ~$6 per troy ounce |

| Silver Peak (Jan 1980) | $50.35 per troy ounce — over 800% rise in ~14 months |

| Silver Thursday Close | ~$10.80 — a 50% single-day crash |

| Hunt Brothers’ Silver Holdings | Est. 200 million troy ounces — approximately one-third of world’s privately held supply |

| Margin Call Received | ~$135 million from broker Bache Halsey Stuart Shields — unable to be met |

| Estimated Losses | Over $1 billion in direct losses; Bunker Hunt declared personal bankruptcy 1988 with debts exceeding $2 billion |

| CFTC Settlement | $134 million in fines (1989) — one of the largest CFTC settlements at the time |

| Rule Change That Triggered It | COMEX Silver Rule 7 (Jan 1980) — prohibited new long positions; traders could only close existing ones |

| M·M·M Lesson | Money — position size as regulatory risk. Method — the exchange controls the game. Mind — conviction in a thesis is not a licence for unlimited size. |

Why Two Billionaires Decided to Buy All the Silver

The 1970s were defined by inflation. After Nixon ended the dollar’s link to gold in 1971, the dollar became a purely fiat currency — backed by faith alone. Through the decade that followed, that faith was severely tested. Oil prices quadrupled. The Vietnam War’s costs fed government deficits. Inflation climbed from 2–3% to double digits. By 1979, the Consumer Price Index was rising at over 13% per year.

For wealthy families who had accumulated capital across generations, this was an existential threat. The purchasing power of a dollar saved in 1971 had been nearly halved by 1979.

Nelson Bunker Hunt’s response: buy silver. The reasoning was not irrational. Silver is finite. It cannot be printed. Throughout history, precious metals have preserved purchasing power across periods of monetary instability. They were not wrong about the logic. They were catastrophically wrong about the scale of the position they built, and fatally wrong about the rules of the game.

Beginning in 1973, they accumulated silver through futures contracts, then by taking physical delivery — demanding actual bullion rather than rolling paper positions. Silver bars flew on chartered aircraft to secure vaults in Switzerland. They were not speculating on a price move. They were engineering one.

By late 1979, partnering with Saudi investors through the International Metals Investment Company, their combined position was approximately 200 million troy ounces — one third of all privately held silver in the world. The silver market had been transformed from a functioning commodity market into an arena with two effectively unlimited buyers on one side and genuine supply tightness on the other.

The Extraordinary Peak: $50 Silver

At fifty dollars per ounce, the effects on the physical market were extraordinary. Industrial users — electronics companies, photographic film producers, jewellers — were paying prices that made their cost structures unworkable. Many switched to alternatives. Many simply absorbed losses and waited.

Tiffany’s ran a full-page advertisement in the New York Times, addressed directly to the Hunt Brothers, accusing them of cornering the silver market and destroying the industry. The first time in memory a major corporation had paid for a national advertisement to criticise specific private individuals by name for their trading activity.

Across America, ordinary people sold family silver. Lines formed outside coin dealers. Dentists received calls from patients asking about fillings. Pawnshops advertised silver buying in their windows. The mania had reached a level of popular participation that few commodity markets ever achieve.

On the COMEX, something dangerous was happening beneath the surface. The Hunts’ positions were so enormous that the exchange faced a genuine question: if contracts came to expiry and delivery was demanded, was there enough silver to actually deliver? This was not theoretical. It was an operational crisis.

In January 1980, the COMEX board acted. Silver Rule 7: no new long positions permitted. Traders could only close existing positions. The mechanism that had been driving prices up — new buying — was suddenly made illegal. The only direction available to the market was down.

The Hunts were trapped.

Silver Thursday: March 27, 1980

Silver had been drifting down for weeks when the margin call arrived. Broker Bache Halsey Stuart Shields demanded approximately $135 million to maintain the Hunts’ positions. They could not meet it.

The default cascaded through the system. Silver fell 50% in a single day — from around $21 to $10.80. The forced liquidation of Hunt positions drove the price down faster than the market had moved in decades. Bache, suddenly holding enormous silver exposure from the Hunt default, faced its own potential catastrophe.

Paul Volcker and the Federal Reserve convened emergency meetings. Banks were quietly encouraged to provide bridge financing to prevent disorderly contagion. The crisis was contained — narrowly.

Silver reached $50 in January. By March 27, it was $10.80. Within months, below $10. Within a year, below $8.

The entire three-year engineering project — the chartered aircraft, the Swiss vaults, the Saudi partnership, the years of patient accumulation — had been undone in weeks. Bunker Hunt’s personal bankruptcy filing in 1988 listed debts exceeding $2 billion. The inheritance of one of the greatest American fortunes had been leveraged into oblivion through a single commodities position.

What This Means for You as a Trader

💰 MONEY — Position Size Creates Regulatory Risk

The Hunts didn’t just face market risk. They faced the risk that a position large enough to threaten market integrity would trigger rule changes. At a certain scale, a position stops being an investment and becomes a systemic problem — and systems respond to systemic problems by changing the rules. The lesson isn’t about silver. It’s that the largest positions in any market carry not just price risk but the risk that the rules governing those positions will change while you hold them. Concentration kills.

📊 METHOD — Know Who Controls the Game

The Hunts were sophisticated. They had a coherent thesis, enormous resources, and a position built over years. What they failed to fully account for was that the COMEX — the exchange on which their futures positions sat — had the power to change margin requirements, position limits, and trading rules while they were holding. In any exchange-traded market, the exchange is the ultimate authority. Any position that requires the continuation of specific rules should account for the risk that those rules change. They always can. Sometimes they do.

🧠 MIND — Conviction Is Not a Risk Framework

The Hunts were right that 1970s inflation was real. They were right that silver had inflation-hedging properties. Their thesis was credible and their analysis was not irrational. None of that was sufficient protection against the leverage, the scale, and the regulatory response their position attracted. Being convinced you are right is not a risk management strategy. At the Complete Trader’s Edge we cap risk at 1% per trade regardless of conviction level — because the history of markets is full of people who were right about the direction and still went broke.

Frequently Asked Questions

What does it mean to “corner” a market?

Cornering a market means accumulating a controlling position in a commodity or asset — large enough that you can effectively dictate the price. In a commodity futures market, a true corner means holding enough contracts that when they come to expiry and delivery is required, there is not enough of the physical commodity available to deliver. Sellers of futures contracts who don’t have the physical commodity must buy it from you — at whatever price you demand — to fulfil their obligations. It is technically possible in illiquid or thinly traded markets; in major commodity markets it is effectively illegal under modern regulations and triggers regulatory intervention, as the Hunts discovered.

Was the COMEX justified in changing the rules mid-game?

This is genuinely contested. The Hunts and their defenders argued that the COMEX board — which included silver dealers and others with significant commercial interests in lower silver prices — changed the rules specifically to damage the Hunts’ position. Supporters of the exchange argued that the position had grown so large it threatened the orderly functioning of the market, and that intervention was necessary to protect all participants. The same debate recurred in 2021 when the LME cancelled nickel trades, and when COMEX faced questions about GameStop-related silver trading. The uncomfortable truth: exchanges have the power to change rules, and that power is inherently subject to the interests of those controlling the exchange.

How did the Hunt Brothers finance such an enormous position?

Through a combination of their own capital, loans from major banks using silver as collateral, and Saudi partnership capital through the International Metals Investment Company. At various points, the banks financing the position included major US financial institutions that were, as silver fell, facing significant losses on their own silver-collateralised loans. This is why the Federal Reserve became involved on Silver Thursday — the potential for a disorderly unwind threatened to spread from a commodities margin call into a broader banking crisis.

Did silver ever recover to anywhere near $50?

Not until 2011, when silver touched approximately $49 per ounce briefly during the post-2008 commodity rally — over thirty years later. It has not reached $50 since. Anyone who bought silver at the January 1980 peak held a losing position for over three decades before getting close to their entry price. This is worth remembering whenever a commodity price rises 800% in fourteen months: the mean reversion potential is as extreme as the initial move, and recovery timescales can be measured in generations.

What is the connection to the LME nickel squeeze of 2022?

The structural parallel is almost exact. In March 2022, Chinese nickel producer Xiang Guangda held a massive short position in nickel on the London Metal Exchange. When Russia’s invasion of Ukraine sent nickel prices spiking 250% in two days — the largest commodity price move in modern history — Guangda faced catastrophic losses. The LME responded by cancelling billions of dollars in trades and suspending nickel trading entirely — a decision even more controversial than the COMEX’s Silver Rule 7, because it retroactively cancelled completed transactions. The episode is covered in Episode 17 of Market Mayhem. The lesson in both cases: the exchange controls the game.

What happened to the silver that the Hunts had physically stored?

The physical silver stored in Swiss vaults and elsewhere was eventually sold by creditors over time as the Hunt Brothers’ debts were worked through. Much of it was sold at prices dramatically below what had been paid for it. The chartered aircraft, the Swiss vault fees, the years of carrying costs — the entire infrastructure of the position added to losses that were already catastrophic. The physical metal that was supposed to protect against the debasement of paper money was ultimately converted back into paper money at a fraction of its peak value.

Continue the Market Mayhem Series

Next: The Stock Market in the Desert

Kuwait, 1982. An air-conditioned parking garage. An unregulated exchange. And $94 billion in postdated cheques in a country of 1.7 million people. The Souk Al-Manakh — the story almost nobody knows.

⚡ Modern Echo · 2026

The Hunt brothers cornered a market, then got cornered by margin calls. In 2026, the cornered market is the S&P 500 itself: seven stocks at 35% of the index, every leveraged fund holding the same names, all facing the same exit door.

Read: The Next Market Crash — 5 Scenarios That Could End the Bull Run →

Market Mayhem is a historical education series produced by The Complete Trader’s Edge. All figures are sourced from historical records. Content is for educational purposes only and does not constitute financial or investment advice. Trading involves significant risk of loss.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →