GREATEST TRADERS · EPISODE 14

Steve Cohen

SAC Capital, the $1.8 Billion Fine, and the Rebirth as Point72

▶ Watch on YouTube🎵 Listen on Spotify

Also available on Apple Podcasts · Amazon Music

Steven A. Cohen

| Born | 11 July 1956, Great Neck, New York |

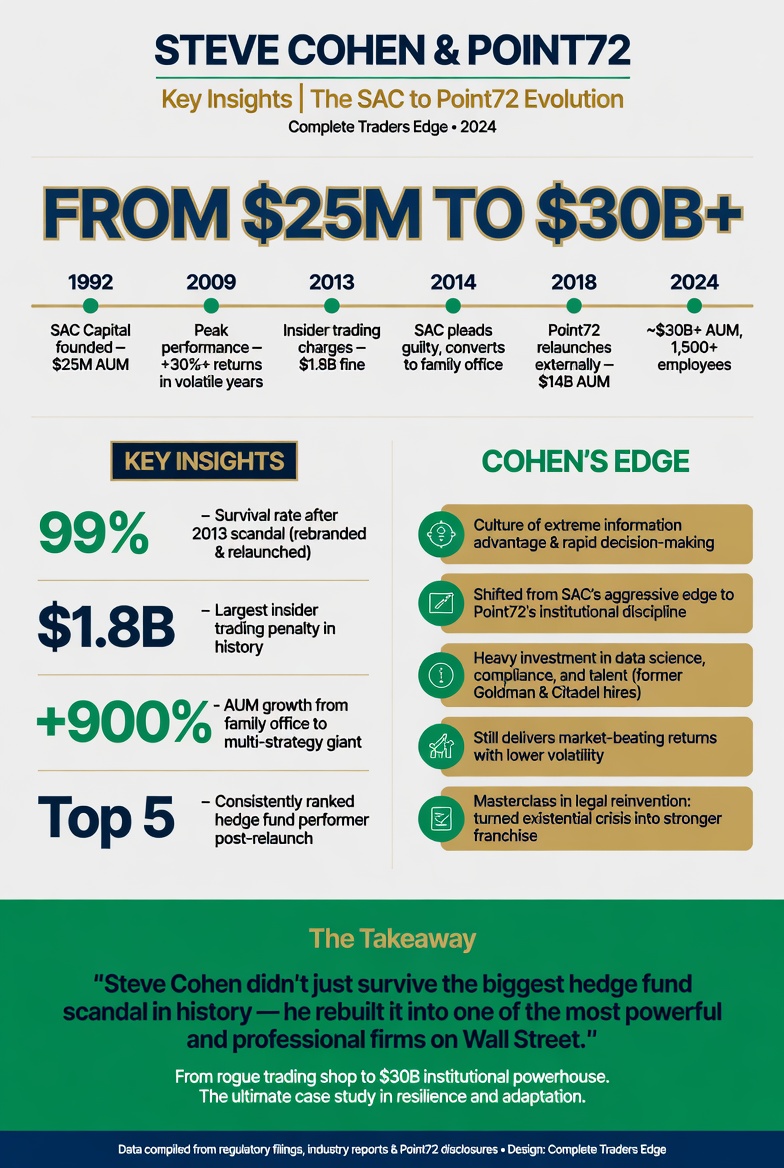

| SAC Capital founded | 1992 (with $25 million) |

| SAC twenty-year average return | ~30% net per year (50% performance fee) |

| SAC peak NYSE volume share | 3% of all daily NYSE turnover |

| SAC 2013 settlement | $1.8 billion fine, guilty plea, fund shut down |

| Cohen’s personal charges | None criminal · SEC civil only (settled 2016) |

| Point72 founded | 2014 (initially family office, reopened 2018) |

| Point72 AUM (2026) | $45.7 billion |

| Net worth (Bloomberg) | ~$14 billion (varies, ~$13-17B range) |

| New York Mets owner since | 2020 |

| Famous quote | “The biggest lesson I learned was: trust but verify. And I didn’t do enough verifying.” |

In November of 2013, the largest hedge fund on Wall Street pleaded guilty to insider trading. SAC Capital Advisors, the firm Steve Cohen had built from $25 million into one of the most feared and most profitable trading operations in history, agreed to pay $1.8 billion in fines, return all client capital, and shut down. The federal indictment described insider trading “occurring over the span of more than a decade, and involving the securities of more than 20 publicly-traded companies.” Eight SAC employees would eventually plead guilty or be convicted at trial.

Steve Cohen himself was never criminally charged. He paid the fine. He gave back the outside money. And in April 2014, he opened a “family office” called Point72 from the same Stamford, Connecticut trading floor SAC had used. He said at SAC’s last Christmas party in 2013, microphone in hand: “We’re going to be the only company that survives a criminal charge from the government.”

By 2026, Point72 manages $45.7 billion. Cohen owns the New York Mets. His personal art collection is estimated at over $1 billion. His net worth sits around $14 billion. The most consequential institutional reorganisation in modern hedge fund history is now the second act in a career that has, by any objective measure, kept compounding.

This is the story of Steve Cohen. The trader whose career averaged thirty percent net returns for two decades, whose firm pleaded guilty to crimes he was personally never charged with, and who survived the kind of regulatory annihilation that ends most Wall Street careers permanently. There is no romanticising this story. It is uncomfortable in places. But it contains lessons about the trader’s craft, the structural pressures of running outside capital, and the difference between an edge and a violation, that no honest trading curriculum should leave out.

Great Neck, poker tables, and the Wharton degree

Steven A. Cohen was born on 11 July 1956 in Great Neck, New York, the third of seven children. His father worked in dress manufacturing on the Garment District side of Manhattan. His mother taught piano. The household was middle-class Long Island, and the kid who would later own a billion-dollar art collection grew up sharing a bedroom with multiple siblings and watching every dollar twice.

Two things shaped his eventual approach to markets. The first was poker. Cohen played in cash games as a teenager and then through college, and he has said in interviews that poker taught him more about probability, risk-taking, and reading people than anything academic ever did. The structural insight of poker, that you do not need to win every hand, that you only need to size your bets correctly relative to your information edge, would become the central operating principle of his trading career.

The second was speed. Cohen was, even as a teenager, fast at math, faster than nearly anyone around him. He could hold prices, ratios, and probabilities in his head while everyone else was reaching for paper. In an era before screens did the calculation work, this was an exploitable advantage. He learned to trust it.

He attended the Wharton School at the University of Pennsylvania and graduated with a degree in economics in 1978. Within days of graduation he was on Wall Street as a junior trader in the options arbitrage department at Gruntal & Co., a mid-tier firm. On his first day on the job, he made a profit of $8,000. By the mid-1980s he was running his own trading group inside Gruntal, generating roughly $100,000 per day, managing a $75 million portfolio with six traders working under him.

By 1992, he was ready to do it for himself. He left Gruntal with $25 million of his own and outside capital and launched SAC Capital Advisors, named after his initials. He was 36 years old.

The SAC machine

SAC was different from the start. Most hedge funds then ran one strategy or one team. Cohen’s structure was the opposite. He hired traders who could each run their own books, gave them capital, gave them constraints, and let them compete inside the firm. The model is now standard in modern hedge funds and is called the “pod” structure or “platform” model. Cohen was not the first to use it, but he was the first to scale it aggressively. By the mid-2000s, SAC had over 100 portfolio managers running independent books inside the firm.

The trading style was rapid-fire. SAC turned over positions quickly. Holding periods were measured in weeks, not years. The information edge came from a combination of fundamental research, technical timing, and what the firm called “mosaic theory,” the practice of assembling small pieces of legally-available information into a complete enough picture to make high-conviction trades.

The performance was extraordinary. From 1992 through the early 2010s, SAC averaged roughly 30% net returns per year. Net of fees that were among the most aggressive in the industry: a 3% management fee and a 50% performance fee, double the standard hedge fund 2-and-20. Investors paid those fees because the after-fee returns still crushed every benchmark in sight.

By 2003, the New York Times reported that SAC was responsible for as much as 3% of all daily trading volume on the New York Stock Exchange. Three percent. From a single firm. The market makers who had to interact with SAC’s flow knew it as some of the most aggressive, best-informed trading in the world. Other funds tried to figure out what SAC was buying and front-run it. The information advantage compounded.

Cohen sat at the centre of it. He had a desk on the trading floor, surrounded by his own monitors. He could see what every portfolio manager was doing. He took the firm’s largest concentrated bets onto his own book. And when he had high conviction, he sized aggressively. The math underneath was the same poker math he had learned as a teenager: edge plus appropriate sizing equals long-term wealth.

The investigation

The first inquiry came in 1986, before SAC even existed, when the SEC suspected Cohen had used inside information to bet that General Electric was about to acquire RCA. The SEC called him to testify. He invoked his Fifth Amendment right against self-incrimination and refused to answer. The investigation eventually closed without charges. The pattern, however, would repeat.

By the mid-2000s, the federal government was building a much larger case. The investigation, run by the Southern District of New York under U.S. Attorney Preet Bharara, focused not just on individual traders at SAC but on whether the firm’s culture systematically rewarded the gathering and use of material non-public information. Mosaic theory, the legal version, requires that the pieces be individually legal. The federal case was that some of SAC’s pieces had been obtained illegally and that Cohen had structurally insulated himself from knowing exactly which pieces.

The most damaging case involved Mathew Martoma, a former SAC portfolio manager who federal prosecutors alleged had received insider information about clinical trial results for an Alzheimer’s drug being developed by Elan and Wyeth. Martoma allegedly relayed the information to Cohen, who reportedly directed the firm to liquidate a $700 million long position and reverse to short before the negative trial results were announced publicly. The trades, prosecutors said, generated approximately $275 million in profits and avoided losses, the most profitable single insider trading scheme in history.

Martoma was convicted in 2014 and sentenced to nine years in prison. He never cooperated against Cohen. Eight other SAC employees either pleaded guilty or were convicted across the broader investigation. None testified against Cohen at trial.

In November 2013, SAC Capital Advisors as an institution pleaded guilty to wire fraud and securities fraud. The firm paid $1.8 billion. It was forced to return all outside capital. It was forced to shut down its investment advisory business. Cohen himself was charged in a parallel SEC civil case with failing to supervise. He settled that case in 2016 by accepting a two-year ban on managing outside money, neither admitting nor denying the allegations. He paid no personal penalty.

The broader question, whether Cohen personally directed insider trading or merely failed to prevent it, has never been resolved publicly. The federal government investigated him for nearly seven years and did not bring criminal charges. He has consistently maintained he had no knowledge of illegal activity at the firm.

The Christmas party and the rebirth

SAC’s last Christmas party in 2013 was held in the lobby of the Stamford headquarters. Reports from people who attended described it as somber. There was no top-shelf scotch. Many of the 1,000-plus employees did not yet know which firm they would be working for in three months.

Cohen took a microphone and proposed a toast. He vowed: “We’re going to be the only company that survives a criminal charge from the government.”

That single sentence, delivered to a room of stunned employees at what felt like the end of an era, is one of the most consequential moments in modern Wall Street history. The conventional wisdom in 2013 was that SAC was finished. The brand was destroyed. The clients were gone. The legal damage was permanent. Most observers expected Cohen to wind down quietly, retreat into his art collection and his Greenwich estate, and disappear from active trading.

He did not. In April 2014, he reorganised the operation as Point72 Asset Management, structured initially as a “family office” managing his personal fortune of approximately $11 billion plus capital from select employees. The trading floor was the same. Most of the senior staff was the same. The strategy was the same. What changed was the compliance infrastructure, dramatically.

Cohen brought in Doug Haynes, a longtime McKinsey partner with prior CIA experience, as president. He hired Vincent Tortorella, a former federal prosecutor, to run compliance. He spent over $100 million on compliance technology, including making Point72 the first asset management firm to license Palantir’s machine-learning software to screen employee communications for red-flag activity. The firm now monitors employee emails for specific patterns, kept secret so traders cannot game the system.

By 2018, the SEC ban had expired and Point72 reopened to outside investors. Cohen later said in an interview that he made roughly 10 to 15 meetings with prospective clients and his staff did the rest, and the firm raised approximately $5 billion in that first year of opening. By 2020, Point72 had raised $10 billion in outside capital and paused additional fundraising. By 2026, the firm manages $45.7 billion.

Cohen, now 69, stepped back from active trading in 2024 after a 40-year career on the desk. He remains co-chief investment officer at Point72 alongside Harry Schwefel, focused on firm strategy, mentoring portfolio managers, and developing talent. He owns the New York Mets and has made the franchise one of the highest-spending teams in Major League Baseball.

What Cohen actually did differently

The temptation with Cohen is to focus entirely on the legal story. The legal story is unavoidable, and any honest profile has to engage with it directly. But it would be incomplete to leave out what made SAC and now Point72 mathematically different from their competitors. There are real lessons here for working traders.

The pod structure. Cohen built a firm where talented portfolio managers competed against each other inside the same risk framework. Each pod ran its own book with its own positions, its own analysts, and its own targets. Capital was allocated dynamically based on performance. Pods that generated returns got more capital. Pods that drew down lost it. The structure meant the firm was simultaneously running dozens of independent strategies, harvesting edge from many different parts of the market at once. The diversification was real because the strategies were genuinely uncorrelated.

Aggressive sizing on conviction trades. Cohen has said in interviews that his single most differentiating trait was the willingness to size up dramatically when a trade had high conviction. Most traders shrink position size when uncertainty grows. Cohen did the opposite when his confidence was high. The poker analogy is exact: when the pot odds are clearly in your favour, you raise, you do not call. The math underneath this is well-established and is the same math that underpins all serious risk management.

Speed and conviction over duration. SAC’s holding periods were short by hedge fund standards. The firm did not hold positions waiting for a thesis to play out over years. It built positions when conviction was high, exited when the thesis was confirmed or invalidated, and moved on. The capital turnover was extraordinary. The implication for retail traders is structural: fast capital with high conviction beats slow capital with low conviction at the level of pure return. The catch is that fast capital with low conviction destroys accounts.

Information infrastructure as edge. SAC and now Point72 spent more on research, data, and analyst relationships than almost any competitor. The premise was that information edge is real, durable, and worth paying for. The firm built relationships with industry analysts, channel-checkers, and primary research providers across hundreds of sectors. The legal version of this is mosaic theory. The illegal version is what got SAC charged. The line between them is real, and it is where the firm crossed it that the federal case eventually focused.

The line between edge and violation

This is the part of Cohen’s story that working traders need to engage with directly, because it is also where the most uncomfortable lessons live.

Information edge is not illegal. Reading more annual reports, talking to more management teams, building better networks, paying for better research, and synthesising more aggressively than competitors are all structurally legal activities, and all hedge funds do them. The federal case against SAC was not that the firm gathered information aggressively. It was that some of the information specific traders relied on came from sources who had a fiduciary duty not to share it, that the firm structurally rewarded the use of that information, and that the supervisory infrastructure failed to detect or prevent the resulting violations.

For a retail trader, the practical implication is that there is a meaningful distinction between aggressive research and material non-public information. Reading a company’s 10-K is research. Calling a contact at the company who is bound by confidentiality and asking them to confirm pre-announcement results is not. The line is bright, even if it is not always obvious in the moment.

The deeper structural lesson is one Cohen himself has stated explicitly. The biggest mistake at SAC, he has said, was insufficient verification. He trusted his portfolio managers to operate within legal lines and did not invest sufficiently in the infrastructure to confirm that they were. Point72 reflects the lesson learned. The compliance investment is now structural and permanent.

For traders running their own capital, the equivalent lesson is simpler. Verify your sources. Verify your data. Verify your edge. Discipline is not just about emotional control during trades. It is also about maintaining clear intellectual hygiene about what you actually know and how you came to know it.

The 2008 crisis and the GameStop sequel

SAC’s record from 2008 deserves specific attention because it cuts against the popular narrative that Cohen’s edge was primarily illegal. In the depths of the financial crisis, when most hedge funds posted catastrophic losses and many liquidated entirely, SAC was reportedly net positive for the year. Cohen has said in interviews that he saw 2008 as one of the great trading opportunities of his career: extreme volatility, dislocated valuations, and forced selling created repeated asymmetric setups where well-capitalised traders with conviction could earn outsized returns. That is not a thesis that requires illegal information. That is a thesis that requires nerve.

In January 2021, during the GameStop short squeeze, Point72 was directly affected. Cohen’s protege Gabe Plotkin ran Melvin Capital, which held large short positions in GameStop and was bleeding badly as the retail-driven squeeze accelerated. Cohen and Ken Griffin’s Citadel together injected $2.75 billion into Melvin to prevent its collapse. Melvin eventually shut down anyway in 2022. Cohen, who also owns the New York Mets, faced public criticism from retail investors over the rescue. His response, characteristically blunt, was that the involvement would not affect his willingness to spend on the Mets.

The episode illustrated something important about Cohen’s networks. He was, by this point, less an active day-to-day trader and more a senior figure in a generation of traders whose careers had passed through SAC. Plotkin was one of dozens. The diaspora of former SAC analysts and portfolio managers now spread across most major hedge funds. The institutional reach of Cohen’s career extends far past Point72 itself.

What Cohen means for your trading practice

Cohen’s career maps onto Mind, Method, Money in ways that are uncomfortable but instructive.

Mind. Cohen’s defining mental trait was decisiveness. When his analysis pointed in a clear direction, he acted at scale. He did not paralyse with doubt or commit half-heartedly. The same poker logic that taught him to fold marginal hands taught him to push large stacks when he had the goods. For a working trader, the lesson is to invest in the analytical work that produces conviction and then act on the conviction when it appears. Half-conviction trades are usually worse than no trade at all.

Method. Build systematic infrastructure for both edge and verification. SAC built infrastructure for edge but failed at verification, and the result was institutional collapse. Point72 rebuilt with both. The trader running their own book needs both too. The edge is the setup, the system, the entry, the exit. The verification is the audit trail of past trades, the journaling, the compliance with your own rules. Without verification, the edge eventually corrupts itself.

Money. Cohen sized aggressively when conviction was high and conservatively when it was not. He understood, perhaps better than anyone of his generation, that the multiplier on a high-conviction trade is what makes a career. Distribution of outcomes matters more than per-trade win rate. A handful of correctly-sized high-conviction trades can produce most of a year’s returns. The job is to be ready when those trades appear, with the analytical work already done and the capital already in position.

The last word

Steve Cohen is now 69 years old. He has stepped back from active trading. He runs Point72 alongside Harry Schwefel and a deep bench of senior portfolio managers. He owns the New York Mets and is reshaping the franchise with the same intensity he once brought to trading. His art collection includes works by Picasso, Pollock, Warhol, Basquiat, Giacometti, and Koons. The Marc Quinn frozen-blood self-portrait that he reportedly displayed in the SAC lobby remains one of the most-talked-about pieces of Wall Street office art in history.

The story of SAC and Point72 is not a clean redemption narrative. The institution he built committed crimes that destroyed the careers of multiple employees and cost shareholders of the affected companies real money. The federal investigation lasted seven years. Eight people pleaded guilty or were convicted. The firm itself ceased to exist in its original form.

And yet, Cohen survived. He paid the fines. He absorbed the reputational damage. He rebuilt with materially better compliance infrastructure than almost any competitor. He kept compounding. By the standards of modern hedge fund history, the second act is now larger than the first.

What Cohen leaves the working trader is something nuanced and worth holding carefully. He leaves a demonstration that aggressive sizing on high-conviction trades, executed within a structure that competes for capital among many strategies, can produce returns that compound at extraordinary rates over decades. He also leaves a demonstration that ambition without sufficient verification produces institutional fragility that eventually breaks.

The honest reading is that both lessons matter. Trading at scale requires both edge and discipline. Cohen had abundant edge. The discipline came later, more expensive than it would have been earlier.

“The biggest lesson I learned was: trust but verify. And I didn’t do enough verifying.” — Steve Cohen

Frequently Asked Questions

Who is Steve Cohen?

Steven A. Cohen is an American hedge fund manager and the founder of SAC Capital Advisors (1992-2014) and its successor Point72 Asset Management (2014-present). He is known for one of the longest sustained track records in modern hedge fund history, with SAC averaging approximately 30% net returns per year for two decades, and for the 2013 federal insider trading case in which SAC pleaded guilty and paid a record $1.8 billion fine. Cohen himself was never criminally charged. He has owned the New York Mets since 2020 and has a personal net worth estimated at approximately $14 billion.

What was SAC Capital and why did it close?

SAC Capital Advisors was a multi-strategy hedge fund founded by Cohen in 1992 with $25 million in capital. By the mid-2000s it managed over $14 billion and was responsible for as much as 3% of all daily trading volume on the New York Stock Exchange. In November 2013, SAC pleaded guilty to wire fraud and securities fraud relating to insider trading by multiple employees. The firm paid $1.8 billion in fines, returned all outside capital, and shut down its investment advisory business. Cohen reorganised the operation as Point72 Asset Management in 2014.

Was Steve Cohen ever charged with insider trading?

No. Cohen was investigated for over seven years by the U.S. Attorney’s office in the Southern District of New York and was never criminally charged. He was charged civilly by the SEC in 2013 with failure to supervise SAC employees who engaged in insider trading. He settled the SEC case in 2016 by accepting a two-year ban on managing outside investor capital, neither admitting nor denying the allegations. Eight SAC employees either pleaded guilty to insider trading or were convicted at trial. Cohen has consistently maintained he had no knowledge of illegal activity at the firm.

What is Point72 Asset Management?

Point72 is the hedge fund Steve Cohen founded in 2014 after SAC Capital pleaded guilty and shut down. It was initially structured as a “family office” managing only Cohen’s personal fortune and capital from select employees. After Cohen’s two-year SEC ban expired in 2018, Point72 reopened to outside investors and raised approximately $5 billion in its first year. As of 2026, Point72 manages $45.7 billion across multiple strategies including discretionary long/short equity, macro, and quantitative. The firm employs over 1,800 people and has invested heavily in compliance and surveillance technology.

What were SAC’s average returns?

SAC Capital averaged approximately 30% net annual returns over its roughly 20-year run, after deducting fees that included a 3% management fee and a 50% performance fee, double the standard hedge fund 2-and-20. The compounded gross returns were higher; the 30% figure is post-fee. The track record placed SAC among the top-performing hedge funds of its era and is part of why federal investigators considered the firm worth seven years of investigation.

What is Point72’s compliance infrastructure?

After SAC’s guilty plea, Cohen invested over $100 million in compliance technology and personnel at Point72. The firm hired Vincent Tortorella, a former federal prosecutor, to run compliance. Point72 became the first asset management firm to license Palantir’s machine-learning software to screen employee communications for red-flag patterns. Specific keywords and phrases are monitored, with the screening criteria kept confidential so traders cannot adapt around them. The firm also conducts regular training, monitors trading activity in real time, and maintains a substantially larger compliance staff than industry peers.

How did Cohen build his fortune?

Cohen built his wealth primarily through his ownership stake in SAC Capital, where he typically retained the largest single position in the firm’s portfolio and earned the largest performance fees. Over two decades of 30% net returns, his personal capital compounded to approximately $11 billion by the time SAC shut down in 2013. After SAC paid the $1.8 billion fine, Cohen’s personal fortune funded the launch of Point72, which has continued to compound. He also holds significant private investments through Point72 Ventures (founded 2014) and assets in art, real estate, and the New York Mets franchise.

Does Cohen still trade?

No. In September 2024, Cohen stepped back from active trading after a 40-year career on the desk. He remains co-chief investment officer at Point72 alongside Harry Schwefel, focusing on firm strategy, talent development, and mentoring portfolio managers. The day-to-day trading is now run by Point72’s portfolio managers across the firm’s multiple strategies. Cohen described the transition as wanting to focus on where he could add the most value at this stage of his career.

Continue Learning

- Linda Raschke: Turtle Soup, the First Market Wizard, and One Losing Year · The pattern trader whose risk discipline ran in the opposite direction from SAC’s aggression.

- Peter Lynch: The Magellan Years and the Method That Made Them · A different model of hedge fund-scale returns through pure fundamentals.

- Charlie Munger: The Latticework Mind That Built Berkshire · Munger’s intellectual humility and verification discipline are the cultural opposite of pre-2013 SAC.

- The Risk of Ruin: Mathematics Every Trader Must Understand · The math behind Cohen’s aggressive sizing on high-conviction trades.

Build Discipline Around Your Edge

Cohen’s career is a study in what aggressive edge can do, and what it costs when discipline lags. The Mind · Method · Money structure in The Complete Trader’s Edge integrates both: edge from concrete setups, discipline from systematic risk management, both reinforced through every chapter.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →