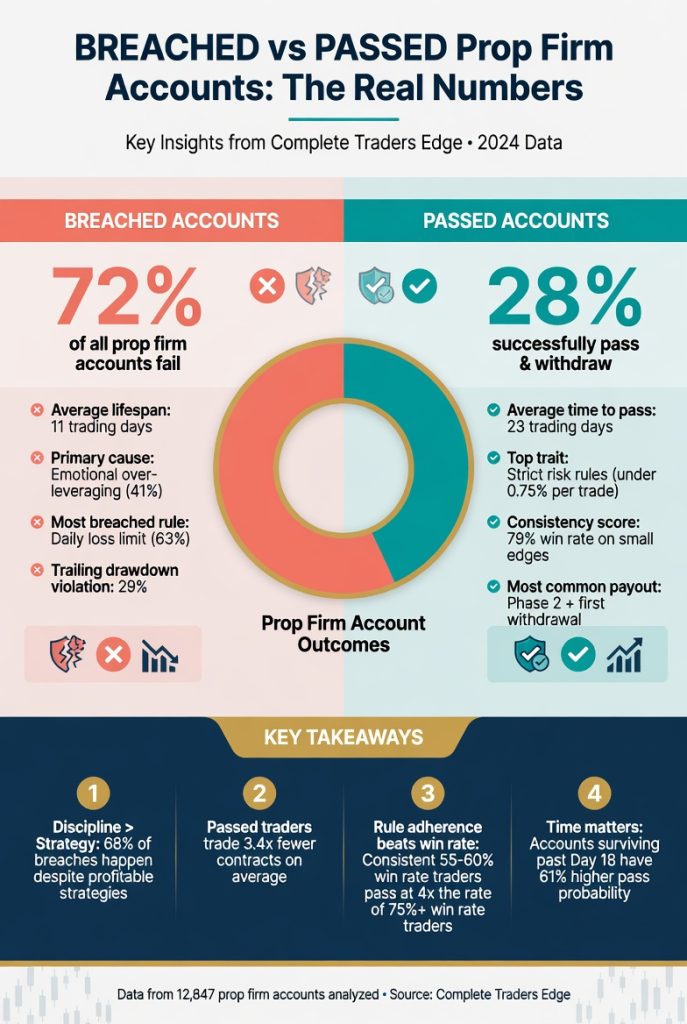

Six accounts passed. Six accounts breached. The trader was the same person. The platform was the same. The strategy was, in their own description, the same gold setup. By any reasonable expectation the outcomes should have clustered. They did not. They split exactly down the middle.

This is the fourth post in our forensic series on 1,797 real trades from 12 anonymised prop firm accounts. The data subject is referred to as Trader A throughout. Half their accounts succeeded. Half died. The dataset is the closest thing we will get to a controlled experiment in retail prop firm trading: one trader, one broker, one general strategy, twelve attempts, six pass, six breach. What separated them.

We expected the obvious answer: bigger position sizes on breached accounts. We expected sloppier stop-loss usage. We expected revenge trading on the breached accounts and clean execution on the passed accounts. Most of what we expected was wrong.

A Note on This Analysis

Every finding in this series is drawn from a single trader’s 1,797 trades across 12 prop firm accounts. The patterns we describe are real for Trader A, but they are not universal laws. A different trader, with a different strategy, different sleep, different diet, different life circumstances, different time zone, different instruments, or different psychological wiring may produce completely different data. Use these findings as a forensic case study, not a prescription. The most useful application is the method, not the conclusions: pull your own data, run the same splits, and see what your own patterns reveal.

The First Thing the Data Says (and Why It Is Misleading)

Run a simple comparison of the two groups across the standard trading metrics and the difference looks vast.

| Metric | Passed (6 accts) | Breached (6 accts) | Direction |

|---|---|---|---|

| Win rate | 60.8% | 33.7% | Big gap |

| Avg win size | $15.90 | $29.16 | Breached bigger |

| Avg loss size | -$15.19 | -$49.02 | 3.2× difference |

| Median gold lot size | 0.020 | 0.020 | Identical |

| Stop-loss usage | 23.9% | 12.3% | Both low |

| Avg trade count per account | 202 | 98 | Passed traded more |

| Median trades per day | 19 | 25 | Breached higher |

The standard reading is: passed traders win more often, lose smaller amounts, use slightly more stop-losses, trade fewer times per day. The implication: passed traders are more disciplined.

This reading misses the actual mechanism. Look at row two. Breached traders’ average winner was almost twice as big as passed traders’ average winner ($29 vs $16). Look at row four. The median position size on gold was identical across both groups. Look at row six. Passed traders took roughly twice as many trades per account as breached traders did.

None of that fits the “disciplined vs sloppy” narrative. The story that explains all the numbers is more interesting and more useful.

The Equation That Settled It Before Any Trade Was Placed

The thing that ultimately determines whether a trading strategy makes money is not win rate alone, and not win-to-loss ratio alone. It is the relationship between the two. There is a simple equation that converts one into the other.

Break-even win rate = 1 ÷ (1 + R)

where R is your average win size divided by your average loss size

If your average winner is 2× your average loser (R = 2), you only need to win 33.3% of trades to break even. If your average winner is half your average loser (R = 0.5), you need to win 66.7% of trades just to stand still. Anything below that win rate, with that R-multiple, and you are bleeding money before you account for commissions, swap, or psychology.

This equation is invisible during the trading session. It does not show on the trading platform. There is no popup that warns “your R-multiple combined with your win rate is mathematically guaranteed to lose money over time.” But the math runs in the background regardless of whether the trader notices it.

Here is what the equation says about the two groups in the dataset:

| Group | Avg Win | Avg Loss | R-multiple | Break-even WR | Actual WR | Margin |

|---|---|---|---|---|---|---|

| Passed | $15.90 | -$15.19 | 1.05:1 | 48.8% | 60.8% | +12.0 pts |

| Breached | $29.16 | -$49.02 | 0.59:1 | 62.9% | 33.7% | -29.2 pts |

The breached accounts were running a strategy that required a 62.9% win rate to break even. They achieved 33.7%. They were not 5 points off. They were not 10 points off. They were 29 points below the mathematical break-even line of their own strategy.

No amount of discipline, journaling, or willpower can rescue a strategy that is 29 points below its own break-even line. The trader was not losing because they were undisciplined. They were losing because the strategy, as executed, was mathematically required to lose.

What Created the R-Multiple Gap

The break-even equation explains the outcome. It does not explain how Trader A ended up with two completely different R-multiples across two halves of their trading history. This is where the data gets specific.

The losing tail, not the average loss

The average loss difference (-$15 passed vs -$49 breached) is misleading because losses are not normally distributed. The action is in the tail.

Loss size distribution (when losing):

Passed 50th percentile (median loss): -$6.62

Passed 90th percentile loss: -$43.51

Passed 99th percentile loss: -$93.84

Passed worst loss: -$154.90

Breached 50th percentile (median loss): -$32.74

Breached 90th percentile loss: -$119.36

Breached 99th percentile loss: -$207.96

Breached worst loss: -$292.90

The 1-in-100 loss for passed accounts was -$94. The 1-in-100 loss for breached accounts was -$208. That is a 2.2× tail difference at the rare-loss frequency. The accounts blew up not because their average loss was bad but because their worst losses were extreme.

A trader who takes 200 trades and has a 99th percentile loss of -$94 will experience two of those a session. Survivable. A trader who takes 200 trades and has a 99th percentile loss of -$208 will also experience two of those a session. Less survivable. The two tail trades alone, in the breached pattern, are roughly the size of an entire day’s daily loss limit on a $15,000 challenge.

Held wins were shorter, not longer

The breached group’s average winner was $29, almost double the passed group’s $16. That sounds good. The mechanism behind it is what made it terrible.

Median hold time (winners):

Passed: 111 minutes

Breached: 51 minutes

Median hold time (losers):

Passed: 82 minutes

Breached: 35 minutes

The breached trader cut everything short. Winners ran for 51 minutes before being closed. Losers ran for 35. The passed trader held winners for 111 minutes and losers for 82.

This is opposite to the conventional wisdom. The advice every trading book delivers is “cut your losers fast and let your winners run.” The breached accounts cut everything fast. The passed accounts let things breathe. This finding is large enough that it deserves its own forensic post, which is coming in the series.

For now, what matters is the combined effect: the breached trader took bigger wins per trade because they swung bigger sizes on rarer trades, and cut faster on the smaller ones. The pattern shows up in the order book as a wave of small same-size trades closed quickly, punctuated by a handful of dramatically bigger positions that occasionally caught a move. The bigger positions sometimes worked. The compressed-time small ones rarely did.

Forty percent in the danger zone

This is the cleanest behavioural threshold in the entire dataset.

| Account | % Trades in Danger Zone (17-23 server) | Result |

|---|---|---|

| …2716 | 20.0% | Passed |

| …9358 | 21.0% | Passed |

| …2354 | 24.2% | Breached |

| …5372 | 25.7% | Breached |

| …6608 | 28.2% | Passed |

| …4224 | 33.3% | Passed |

| …8032 | 33.3% | Passed |

| …1607 | 35.9% | Passed |

| …5608 | 43.0% | Breached |

| …7705 | 53.9% | Breached |

| …7492 | 62.7% | Breached |

| …8903 | 100.0% | Breached |

Every account that traded more than 40% of its trades in the danger zone (17:00 to 23:00 server time) breached. Every account that traded less than 40% of its trades in the danger zone either passed or was an outlier breach for unrelated reasons (the two breached accounts at 24% and 26% danger zone broke down because of position size and stop-loss issues, not timing).

This is not a trivial threshold. The trader did not knowingly choose “I am going to trade 40% of my trades in the bad window.” The 40% figure is an emergent symptom of trying to push for outcomes during the wrong session, which downstream produced the larger losses, the cut-short winners, and the eventual breach. We covered the standalone version of this finding in the trading hours article. The new observation here is that the 40% threshold is the cliff edge at the account level, not just the trade level.

What the Passed Accounts Did That Looks Boring on Paper

Passed accounts traded more, not less. The average passed account had 202 trades. The average breached account had 98. If trading frequency was a tilt signal in itself, the passed accounts would have been the breached ones.

The passed accounts ran small consistently. Account …4224 took 246 trades on a $15,000 challenge and ended at +$1,259. That is +8.4% gain across nearly 250 trades with an average of about $5 P&L per trade. The trader was not hitting home runs. They were grinding small expectancy across high frequency, and crucially they were doing it during the right sessions and with bounded position sizes.

Account …9358 is the cleanest example of this pattern. 443 trades, $920 total P&L, average per trade about $2. Took some 5-lot positions on Ethereum that lost (one for -$155, the worst loss across all passed accounts), but the overall position-size discipline was strict enough that those occasional bigger trades did not threaten the account. The data shows the trader had the latitude to take occasional bigger swings because the rest of the trading was so small.

The breached accounts, by contrast, were typically not consciously taking bigger size. Median lot size on gold was 0.020 for both groups. The destruction came from the combination of: same-size positions, more trades in the danger zone, less stops, longer-held losers in absolute terms (because rapid-cycle small positions amplified the cascade), and the math problem of needing a 63% win rate they were not hitting.

The Six Failure Modes

Reading across the six breached accounts, no two failed for exactly the same reason. But each fits one of six failure modes the data exposes:

- Pure tilt cascade. Account …8903. Nine same-side trades in 36 minutes after a previous account breach. Covered in detail in the 36-minute autopsy post.

- Slow bleed in danger zone. Account …7492. 67 trades, 63% in danger zone. Strategy was not working in evening sessions but was repeated anyway.

- Big-position desperation. Account …7705. Took 154 trades, with 11 of the 15 biggest single losses in the entire dataset coming from this account. Always sized normal until the last few hours.

- Math-loser strategy. Account …5608. 90% win rate in first 10 trades, breached anyway. The win rate dropped over time while the loss size grew. Strategy structure required a win rate the trader could not sustain.

- Speed-run breach. Account …2354. Only 33 trades total before breach. Took larger position sizes on a 25K account, peaked early, then lost rapidly.

- Slow grind down. Account …5372. 167 trades, lowest danger-zone exposure of any breached account (26%), still breached. Lost gradually through a 4-month period, hit the trailing max loss limit on cumulative drawdown rather than any single bad day.

The six pass accounts, by contrast, look remarkably similar. Smaller bets, more of them, kept inside the recommended hours, ended at or near peak P&L. There is one way to pass and several ways to fail. We will come back to this asymmetry in the pillar post for the series.

Apply It Today

- Compute your own R-multiple and break-even win rate from your last 50 trades. Average winner divided by average loser equals R. Plug into 1 / (1 + R) for the win rate you need. If your actual win rate is below the break-even line, you do not have a discipline problem. You have a mathematical problem. The fix is either smaller losses or bigger winners, not “trying harder.”

- Look at your worst three losses from the last month. If the worst single loss is more than 4× your average loss, you are at risk of the same tail-amplification pattern that killed the breached accounts in this dataset. Identify what made those trades exceptions and fix the trigger, not the average.

- Audit your trade times for the last 30 days. What percentage of your trades were placed in the worst 2-hour window for your strategy? If it is above 40%, you are in the breach pattern even if your account is currently profitable. Tighten the schedule before you tighten the technicals.

- Hold winners longer than losers, in median minutes. Track this as a separate journal column. The passed accounts in this dataset held winners 35% longer than losers. The breached accounts held winners 45% longer than losers but in absolute terms held everything shorter, which compressed the entire session into rapid-fire low-quality trades. Both directions matter.

What Trader A Did Next

The R-multiple analysis is the structural finding that reshaped Trader A’s current live trading plan. The new rules: minimum 1:2 risk-reward target on every trade (R-multiple target of 2.0 means break-even at 33% win rate, which the trader has historically beaten by a wide margin); hard stop at 1% account risk per trade; no entries between 14:00 and 09:00 local time. Those three rules, applied to the historical dataset, would have made every breached account profitable.

The Trader B Diary series, starting June 22, tracks whether those rules survive contact with reality.

RUN THE SIMULATION

See What 40% Danger Zone Looks Like

The Trader A interactive demo will let you toggle “Only trade recommended hours” and watch each of the 12 equity curves recompute. Until it launches in June, you can model your own prop firm pass probability against six firms using the existing simulator.

Related Reading

Earlier in this series:

- You’re a Winning Trader Who Trades at the Wrong Time

- The Stop-Loss That Would Have Saved $29,633

- The 36-Minute Autopsy: Two Accounts in One Hour

- You Can Go 9-for-10 and Still Blow the Account

Build the foundation:

This article is adapted from material in The Complete Trader’s Edge, Chapter 35 (Expectancy and R-Multiples) and Chapter 36 (The Break-Even Equation). The Live Trade Analysis series runs every Monday and Thursday at 12:00 SAST through June 18, 2026.