Market Mayhem · Episode 10 · 1989–2024 · Japan

The Sun Also Falls

Japan’s Lost Decades: The Market That Took 35 Years to Recover

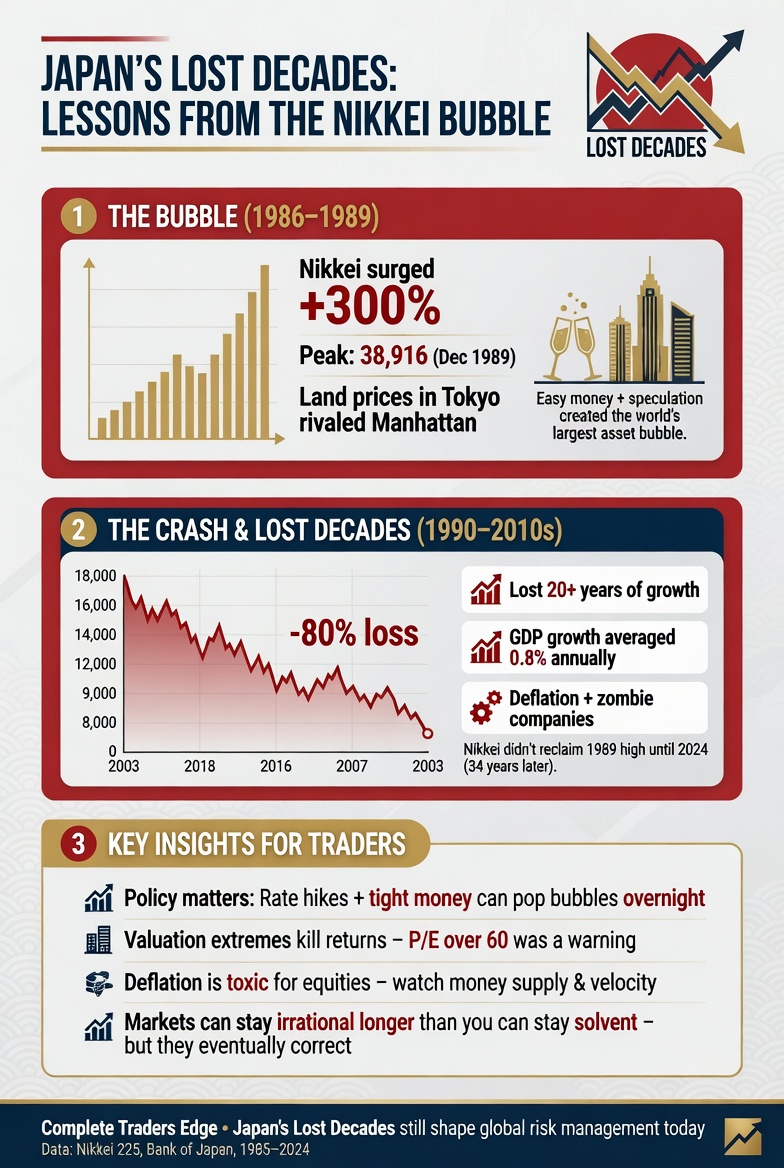

Nikkei 38,915 on December 29, 1989. The same level reached again in 2024. “Markets always come back” — but not always within your lifetime.

On December 29th, 1989 — the last trading day of the decade — the Nikkei 225 closed at 38,915 points.

The grounds of the Imperial Palace in central Tokyo were valued, by some estimates, at more than all the real estate in the state of California. Golf club memberships near Tokyo cost the equivalent of millions of dollars. Japanese corporations were buying Rockefeller Center, Columbia Pictures, and Pebble Beach Golf Course. Japan was the consensus pick for the dominant economy of the twenty-first century. The question was not whether Japan would surpass America. It was when.

Four trading days later, the Nikkei began to fall. By 2003, it had lost more than 80% of its peak value. By the time it returned to 38,915, it was 2024.

Thirty-five years. The most complete demolition of the “markets always come back” assumption in the history of modern finance.

The Crisis at a Glance

| Data Point | Detail |

|---|---|

| Event | Japan asset price bubble collapse and Lost Decades |

| Nikkei Peak | 38,915 — December 29, 1989 |

| Nikkei Trough | ~7,700 — April 2003 — an 80% decline over 13 years |

| Recovery to Peak Level | 2024 — 35 years after the original peak |

| Japanese Real Estate (1989) | Estimated at ~4× the total value of all US real estate; Imperial Palace grounds valued at more than all California |

| Nikkei P/E Ratio at Peak | 60–80× earnings — historically extreme by any conventional valuation standard |

| Tokyo Stock Exchange Peak | ~45% of world’s total equity market capitalisation — from a single city |

| Key Trigger | Bank of Japan rate tightening beginning 1989, unwinding the cheap money that had inflated asset prices |

| Banking System | “Zombie banks” — carrying non-performing loans at fictional valuations rather than recognising losses |

| Social Consequence | Lost generation, wage stagnation, deflation spiral, hikikomori phenomenon of economic withdrawal |

| Policy Error | Regulatory forbearance — allowing zombie banks to function rather than forcing recognition of losses and recapitalisation |

| M·M·M Lesson | Money — “markets always come back” is not a law. Method — credit-backed asset bubbles unwind through the banking system. Mind — universal consensus is the danger signal, not the safety signal. |

The Miracle and Its Hidden Architecture

Japan’s post-war recovery had been genuinely extraordinary. A country devastated by defeat and atomic bombs had rebuilt itself into the world’s second-largest economy in three decades. Toyota. Sony. Honda. Canon. Companies that had started from nothing in 1945 and built world-class global positions. The success was real, the companies were real, the manufacturing excellence was genuine.

But through the 1980s, a structural change was occurring that was invisible in the aggregate statistics. It began with the Plaza Accord of 1985, when the G5 agreed to weaken the US dollar and strengthen the yen — a fifty percent appreciation that devastated Japan’s export competitiveness. The Bank of Japan cut interest rates aggressively to offset the export slowdown. Money became extraordinarily cheap.

The cheap money flowed not into productive manufacturing investment but into real estate and equities. Japanese accounting rules allowed corporations to count unrealised gains on equity holdings as capital. As stocks rose, balance sheets appeared stronger, enabling more lending, which drove stocks and property higher, generating more paper gains, which appeared as more capital, enabling more lending still.

The circularity was complete and self-reinforcing — and it would only stop when asset prices stopped rising. In 1989, the Bank of Japan raised rates to address the inflation the cheap money had created. It set in motion a thirty-five-year unwind.

The Numbers That Defined a Peak

Total Japanese real estate in 1989: estimated at four times the value of all US real estate, in a country the size of California. The Nikkei’s price-to-earnings ratio: 60–80 times, consistent only with growth rates no real economy sustains. Tokyo Stock Exchange market cap: approximately 45% of global equity market capitalisation from a single city.

Japanese corporations, their balance sheets inflated by paper gains, were buying the world with leverage: Rockefeller Center for $846 million, Columbia Pictures for $3.4 billion, Pebble Beach Golf Course for $841 million. Trophy acquisitions by companies whose apparent financial strength was itself an artefact of prices that were about to collapse.

The cultural certainty was total. Japan had found a better model. Books were written. Corporations sent executives to learn Japanese management techniques. The question being seriously discussed in 1989 was not whether Japan would surpass the United States economically, but when.

The Unwind: Thirteen Years Down, Twenty-Two More to Recovery

The Nikkei’s decline from December 1989 was not a sharp, single-event crash. It was a prolonged unravelling — which made it psychologically more devastating than any sudden collapse. Each year brought hope of recovery. Each recovery attempt eventually failed. By 1992: down 60%. By 2003: down 80%.

The banking system’s response amplified everything. Japanese banks carried non-performing loans — loans to real estate developers whose collateral was now worth a fraction of what they had borrowed — at valuations that bore little relationship to reality. Rather than recognise the losses (which would have required recapitalisation or insolvency for some institutions), regulators allowed the banks to carry the fiction on their books. The zombie banks continued to exist, neither lending normally nor failing formally. They simply occupied space in the financial system, unable to fulfil their core function of allocating capital to productive use.

Deflation set in — the specific trap Japan fell into where declining prices discouraged spending and investment, because tomorrow things would be cheaper. Deflation is extraordinarily difficult to escape once entrenched. Japan’s experience with it shaped global central bank policy: the terror of deflation is one reason why the Fed, ECB, and Bank of England responded to 2008 with such aggressive monetary expansion.

The Nikkei eventually returned to 38,915 in 2024. A fifty-year-old investor at the 1989 peak was eighty-five at recovery. For most people who invested at the top, the waiting was longer than their investment horizon.

What This Means for You as a Trader

💰 MONEY — “Markets Always Come Back” Is Not a Law

The Nikkei returned to its 1989 high in 2024 — thirty-five years later. A Japanese investor who was fifty in 1989 was eighty-five at recovery. “Buy and hold” requires the specific condition that the price you paid is not so disconnected from underlying value that recovery takes a generation. Valuation matters. Paying any price for any asset on the assumption that time will rescue you is not an investment strategy. It is hope dressed in investment language. Always know the valuation you are paying, and what that implies about the recovery time if the thesis takes longer to play out than expected.

📊 METHOD — Credit-Backed Bubbles Unwind Through the Banking System

Japan’s bubble was not just equity overvaluation. It was a credit bubble: rising asset prices used as collateral to support loans that funded more asset purchases. When prices fell, they destroyed collateral, which impaired loans, which forced selling, which drove prices lower. The unwind was amplified, not proportional. Understanding the credit structure beneath any asset market — how much of its price is supported by lending against itself — is essential to understanding its vulnerability. The higher the credit leverage underpinning an asset’s price, the more violent the potential unwind when the trend reverses.

🧠 MIND — Universal Consensus Is the Danger Signal

In 1989, Japan’s dominance was the consensus view of the global financial community. Not just a majority view — a consensus so complete that being sceptical felt absurd. When every analyst agrees, when every book confirms the same thesis, when asking “what if the trend reverses?” feels unnecessarily contrarian — that universality of confidence is a warning sign, not reassurance. The most dangerous position is the one that everyone agrees is safe. The most important question to ask is the one that feels most unnecessary to ask. Especially then.

Frequently Asked Questions

Why did the Nikkei take 35 years to recover when other markets recovered much faster?

Several compounding factors. The initial valuations were extreme — 60–80× earnings — meaning the gap between price and underlying value was enormous, requiring either decades of earnings growth or continued price decline to close. The deflationary spiral that followed depressed corporate earnings. The zombie bank problem prevented the normal credit cycle from functioning, choking off capital allocation and growth. Regulatory forbearance kept the financial system impaired rather than forcing the painful but necessary recognition and resolution of losses. And Japan’s demographic challenge — a rapidly ageing and declining population — created a structural headwind to economic growth that persisted regardless of policy. No single factor explains thirty-five years; all of them together do.

What are “zombie banks” and why were they such a problem?

Zombie banks are financial institutions that are technically insolvent — their assets are worth less than their liabilities — but that continue to operate because regulators allow them to carry those assets at fictional valuations rather than requiring mark-to-market accounting. They are “undead” — not functioning properly but not formally failed. The problem: zombie banks cannot lend normally because their capital base is fictitious; cannot fail normally because regulators won’t force it; and cannot recapitalise normally because no rational investor will put money into an institution whose true balance sheet they cannot assess. They occupy space in the financial system without performing the function of a healthy financial institution. Japan’s zombie bank problem lasted for most of the 1990s and contributed significantly to the prolonged stagnation.

What lessons did global policymakers take from Japan’s experience?

The US response to 2008 was shaped significantly by Japan’s Lost Decade experience. The Fed’s aggressive quantitative easing reflected the determination to prevent deflation that Japan failed to prevent. The forced recapitalisation of US banks — requiring them to raise capital and write down losses — reflected the lesson that regulatory forbearance and zombie banks were more damaging than the short-term pain of forcing institutions to confront their true position. The explicit inflation targeting adopted by central banks globally reflected the understanding that deflation, once entrenched, is extremely difficult to escape. Japan’s failure to act decisively when its banking crisis began in the early 1990s became the primary case study for how not to manage a post-bubble financial crisis.

What is the hikikomori phenomenon and how is it connected to the Lost Decades?

Hikikomori refers to individuals — predominantly young men — who withdraw completely from social and economic participation, remaining isolated at home for months or years. The phenomenon emerged as a significant social issue in Japan during the Lost Decades. While it has multiple causes (cultural, psychological, social), its emergence and scale during a period of prolonged economic stagnation that offered limited opportunities to young people entering the workforce is not coincidental. A generation of Japanese young adults found that the economic promise available to their parents — stable employment, rising wages, the prospect of middle-class security — was simply not available to them. Some responded by withdrawing. Estimates of the total number of hikikomori at various points ranged from hundreds of thousands to over a million individuals.

Could a Japan-style Lost Decade happen in Western markets?

The specific combination of factors that created Japan’s thirty-five-year stagnation — extreme initial valuations, credit-backed bubble, zombie bank regulatory forbearance, demographic decline, deflationary spiral — is difficult to replicate exactly in most Western contexts. However, elements of it are not impossible. Extended periods of low or no real returns from equity markets that are significantly overvalued at the point of purchase are historically not unusual. The US stock market of the early 2000s, bought at peak dot-com valuations, delivered negative real returns over the following decade. The lesson is not that the Nikkei experience will repeat exactly in another market. The lesson is that paying extremely high valuations for assets, in an environment of credit-backed price inflation, creates recovery horizons that can exceed any individual’s practical investment horizon.

What is the single most important takeaway for a long-term investor?

The price you pay is the primary determinant of your long-term return. Not the quality of the underlying asset — Japan’s best companies were, and remain, genuinely excellent. Not the growth of the economy — Japan’s economy did eventually resume some growth. The price. When you buy an asset at 80× earnings, you are making a claim about future growth rates that reality may or may not validate, and if reality does not validate it, the time required to recover your investment at more reasonable valuations may exceed your investment horizon. Valuation is not the sexiest investment concept. It is the most important one. The Nikkei’s thirty-five-year recovery is the proof.

Continue the Market Mayhem Series

Next: Tequila Hangover — The Mexican Peso Crisis

1994. Mexico was the poster child of emerging market optimism. NAFTA had just been signed. Then the peso was devalued — and in 48 hours, a decade of confidence evaporated.

Market Mayhem is a historical education series produced by The Complete Trader’s Edge. All figures are sourced from historical records. Content is for educational purposes only and does not constitute financial or investment advice. Trading involves significant risk of loss.