Market Mayhem · Episode 04 · 1840s · United Kingdom

Iron Horses and Paper Fortunes

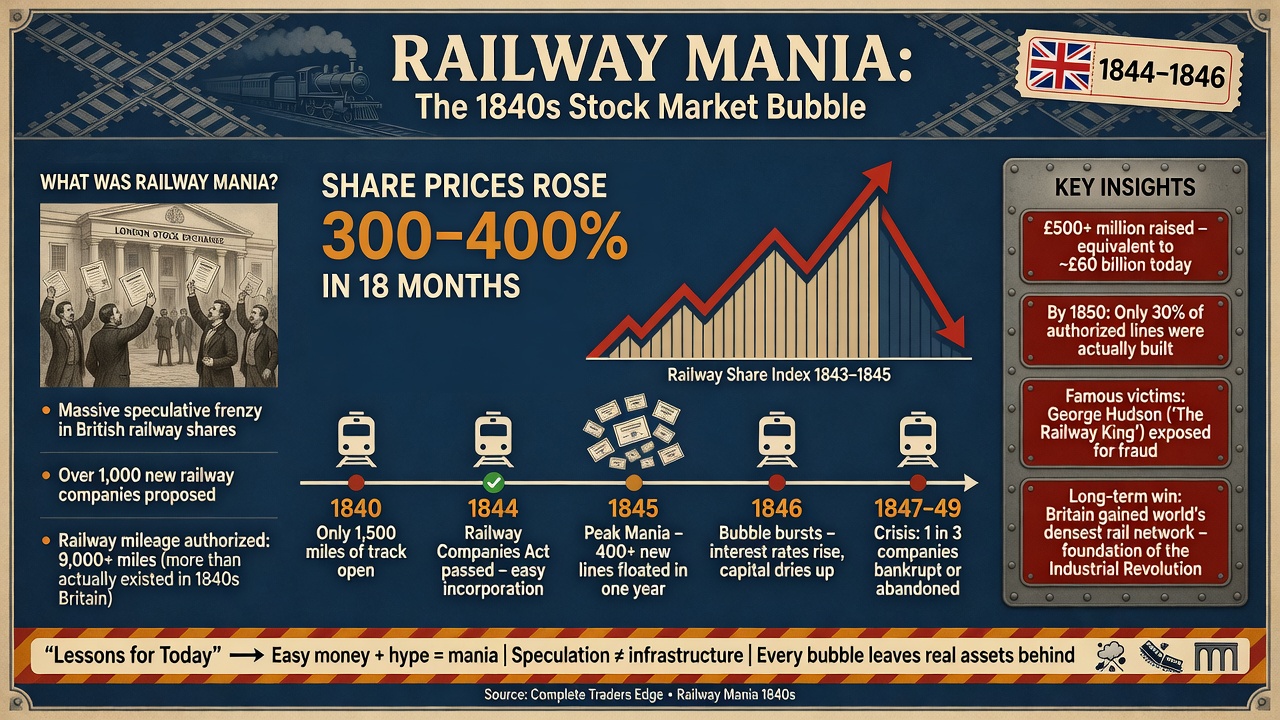

The Railway Mania of the 1840s: When Britain Bet Its Future on Steam

The Brontë sisters invested. Parliament voted on its own portfolio. And the most powerful businessman in Britain was running the greatest fraud of the century.

▶ Watch on YouTube🎵 Listen on Spotify

Also available on Apple Podcasts · Amazon Music · iHeart Radio

📄 Free Download · Episode Research Sheet

Railway Mania Research Sheet (PDF)

The full timeline, key numbers, the Mind, Method, Money lessons, and further reading from this episode. Free, no email required.

The railroad was the most transformative technology of the nineteenth century. It was not a fantasy. It was not a story. It was iron and steam and engineering genius that compressed geography, created national economies, and permanently altered what it meant to live in an industrialised society.

It was also the vehicle for one of the most spectacular speculative manias in history. A bubble that consumed the savings of factory workers and literary geniuses alike. That produced two hundred and seventy-two railway acts in a single year of parliamentary insanity. That elevated a linen draper’s apprentice named George Hudson to the pinnacle of British society — and then destroyed him completely when his accounts were finally examined.

The technology worked. Most of the investments didn’t. This is the most important distinction in the history of markets.

The Crisis at a Glance

| Data Point | Detail |

|---|---|

| Event | Railway Mania — mass speculative investment in British railway companies |

| Location | United Kingdom, primarily England |

| Peak Year | 1845 — the apex of new company floatation and parliamentary approval |

| Railway Acts (1846 alone) | 272 acts passed, authorising 9,500 miles of new track in a single year |

| Capital Committed (est.) | £200–500 million — approaching Britain’s entire annual national income |

| Lines Never Built | Approximately one-third of all approved lines were never constructed |

| Key Figure | George Hudson — “The Railway King.” Controlled ~30% of England’s rail network. Later exposed as a systematic fraudster. |

| Notable Investors | Charlotte, Emily and Anne Brontë (£500 in York and Midland Railway); Members of Parliament; the Duke of Wellington’s circle |

| Collapse Trigger | Bank of England rate rise (Oct 1845) + investigative journalism in The Times + capital calls exceeding investor capacity |

| Hudson’s Fraud | Paying dividends from capital raised from new investors; concealing land purchases; self-dealing on contracts |

| Legislative Legacy | Contributed to development of accounting standards and the Companies Act 1862 — foundation of modern corporate law |

| M·M·M Lesson | Method — technology ≠ investment. Money — hidden obligations in call structures. Mind — charisma as a substitute for analysis. |

The Technology That Actually Changed the World

The Liverpool and Manchester Railway opened in 1830 — the world’s first inter-city passenger railway, powered by steam. On its opening day, William Huskisson, a Member of Parliament, stepped in front of Stephenson’s Rocket and became the first railway fatality in history. Even the origin had drama.

But what the railway did to the world was genuinely revolutionary. Before it, the fastest overland travel was a horse. London to Edinburgh took two days in good conditions. The railway changed all of it. London to Edinburgh in eight hours. Fresh fish to inland markets overnight. Industrial goods moving at costs that made entirely new economic models viable.

The trunk lines of the 1830s — the Great Western, the London and Birmingham, the Midland — were genuinely profitable. Their shareholders received real dividends from real operations. And this documented, dividend-paying reality was the seed of the disaster that followed. Because if the early lines are profitable, more lines must also be profitable. If more lines are profitable, more still must be more profitable again. The logic seemed sound. It was catastrophically wrong.

The early lines were profitable because they were natural monopolies connecting large population centres with no alternative. The five thousand new lines proposed during the mania were something entirely different: duplicating existing service, crossing expensive terrain, promoted by people who had identified investor appetite rather than genuine demand.

The Railway King

George Hudson controlled nearly a third of all operating English rail lines. He dined with the Duke of Wellington. He was twice elected Lord Mayor of York. He delivered returns, quarter after quarter, year after year, while the rest of the industry was still burning capital. Nobody asked how.

He was paying dividends from capital: taking money raised from new investors and distributing it to old ones as profit. Manufacturing the appearance of profitability in companies that were still spending far more than they earned. As long as new money kept coming in and nobody examined the accounts, the machine kept running.

Parliament was simultaneously approving his schemes with a spectacular conflict of interest. Members sat on select committees evaluating railway viability while holding railway shares. They were not assessing public benefit. They were voting on their own portfolios. The result: two hundred and seventy-two railway acts in 1846 alone, authorising nine thousand five hundred miles of new track.

The Collapse

In October 1845, the Bank of England raised interest rates. Capital that had flooded into speculative railway shares now had alternatives. Investors started calculating. The numbers on many companies were deeply unconvincing.

The structural trap was devastating. Investors hadn’t paid full price upfront — they had put down deposits of around ten percent, with calls due later as construction required capital. In a falling market, this created obligations exceeding the value of what they owned. Many refused to pay calls. Many couldn’t. By 1847, hundreds of companies had suspended. The crash spread from railways into the broader credit system.

The Brontë sisters lost most of their £500. George Hudson, exposed in 1849 by shareholders who finally examined his accounts, was systematically destroyed. His wealth seized. His political career ended. He fled to France to escape his creditors. The Railway King’s empire revealed as an elaborate and ultimately ruinous performance.

What This Means for You as a Trader

📊 METHOD — Technology Is Not a Valuation

Railways changed the world. Most railway shares went to zero. The internet changed the world. Most dot-com shares went to zero. AI is changing the world right now. The companies that survive will be extraordinary investments. The ones riding enthusiasm without viable economics are the Railway Mania investments of our generation. Separate the technology from the company. What are the revenues? What is the path to profitability? The excitement does not change the math.

💰 MONEY — Know Your Total Exposure Before You Enter

Railway investors lost not just what they had invested but what they had committed to invest later. The call structure created obligations that materialised in the worst possible conditions. Modern leveraged positions work identically — the margin call arrives when the market is most volatile and liquidity is thinnest. Know your maximum possible obligation before you enter, not when the call arrives.

🧠 MIND — Charisma Is Not Evidence

George Hudson delivered consistent returns while others struggled. This made him trusted beyond rational basis. Admiration for consistent performance — especially when others are losing — creates a psychological block against the obvious question: how? Returns without a clear, verifiable explanation deserve scrutiny, not deference. The person delivering miraculous results most reliably is the person most worth examining most carefully.

Frequently Asked Questions

Did the railways themselves succeed, despite the mania?

Yes — and this is the defining irony. The technology worked completely. The surviving railways went on to transform Britain and eventually the world. Lines like the Great Western Railway still operate today substantially along their original routes. The investors who backed the wrong companies at the wrong prices lost everything. The technology itself was one of the most successful innovations in human history.

Why did the Brontë sisters invest in railways?

Charlotte, Emily, and Anne Brontë invested approximately £500 in the York and Midland Railway in 1845. They were not naive — they were rational people doing what almost every rational person around them was doing. Early railway investors had received genuine dividends. The case for railway investment, based on available evidence, was credible. They lost most of what they put in.

How did George Hudson’s fraud actually work?

Hudson paid dividends from capital rather than from genuine earnings — taking money from new investors and distributing it to existing shareholders as “profit.” He also concealed land purchases, awarded contracts to himself at inflated prices, and manipulated accounting across multiple companies. When shareholders’ committees examined his books in 1849, the fraud was found to be extensive, systematic, and long-running. He was not prosecuted — corporate fraud law was still developing — but he was financially destroyed.

What is the modern equivalent of the Railway Mania?

The dot-com bubble of 1995–2000 is the closest structural parallel. Both involved a genuinely transformative technology that attracted enormous speculative capital far in excess of any realistic near-term earnings potential. Both produced companies built on stories rather than revenues. Both saw the technology ultimately succeed while most individual investments failed. The current enthusiasm around artificial intelligence has similar structural characteristics.

What is a “call” in railway investment, and why was it so dangerous?

Railway shares were not paid for upfront. Investors put down a deposit of around ten percent, with the balance due in instalments called “calls” as construction required capital. In a rising market this created leverage. In a falling market, it created obligations exceeding the value of what investors owned. When prices collapsed below the call price, investors were being asked to pay more than market value for assets they couldn’t sell. Many defaulted. Many were ruined not by their initial investment but by the commitments they had made when prices were rising.

What is the single most important lesson for a modern investor?

Separate the technology from the investment. This requires active, conscious effort because enthusiasm for a genuinely transformative technology creates powerful psychological pressure to conflate the two. The question is never “is this technology real?” In a mania, it usually is. The question is: “Is this specific company, at this specific price, with these specific economics, a sound investment?” That question has the same answer in a technology revolution as in any other market. It requires the same rigour. It rewards the same patience.

Continue the Market Mayhem Series

Next: Black Tuesday — The Day America Stopped Believing

1929. Margin lending. The greatest crash in American history. And Jesse Livermore — who shorted it perfectly and made $100 million — then lost everything.

⚡ Modern Echo · 2026

Railway Mania was “this technology will reshape civilisation” priced as if it could only be right. It did reshape civilisation. The stocks still crashed 85%. In 2026, AI is the railways, and the circular financing between Nvidia, OpenAI, Microsoft and Oracle is the same shape, twenty zeros bigger.

Read: The Next Market Crash — 5 Scenarios That Could End the Bull Run →

Market Mayhem is a historical education series produced by The Complete Trader’s Edge. All figures are sourced from historical records. Content is for educational purposes only and does not constitute financial or investment advice. Trading involves significant risk of loss.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →