Market Mayhem · Episode 03 · 1720 · United Kingdom

The Bubble That Broke Britain

“I can calculate the motions of heavenly bodies, but not the madness of people.”

— Isaac Newton, 1720. After losing £20,000 in the South Sea Bubble.

▶ Watch on YouTube🎵 Listen on Spotify

Also available on Apple Podcasts · Amazon Music · iHeart Radio

📄 Free Download · Episode Research Sheet

The South Sea Bubble Research Sheet (PDF)

The full timeline, key numbers, the Mind, Method, Money lessons, and further reading from this episode. Free, no email required.

In the summer of 1720, Isaac Newton — the man who explained gravity, invented calculus, and mapped the orbit of every known planet — stared at a trading ledger and confronted the one force he had never been able to quantify.

He had just lost £20,000. In today’s money, somewhere between two and four million pounds. Not because he was uninformed. Not because he hadn’t done his research. But because he had watched everyone around him getting rich, held out as long as any rational person could, and then — at the very top of one of the most spectacular financial manias in history — bought back in with everything he had.

The South Sea Bubble of 1720 is the most important story in the history of speculative markets. Not because of its scale. Not because of the political corruption it exposed. But because of what it tells us about the one enemy that no intelligence, no experience, and no analytical framework can fully defeat.

The enemy is watching. Watching while others get rich. And eventually being unable to watch anymore.

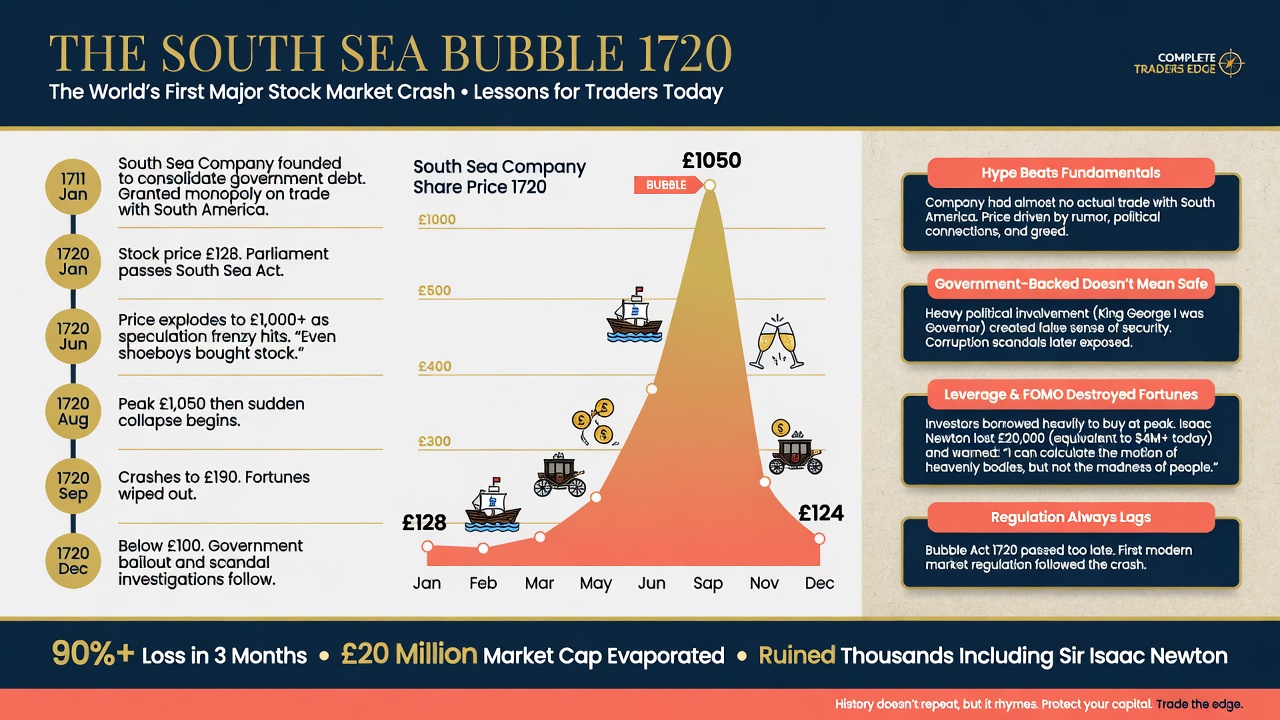

The Crisis at a Glance

| Data Point | Detail |

|---|---|

| Event | South Sea Company speculative bubble and collapse |

| Location | London, United Kingdom — centred on Exchange Alley |

| Share Price (Jan 1720) | £128 per share |

| Share Price (Peak, Aug 1720) | Over £1,000 per share — an 800% rise in 8 months |

| Share Price (Dec 1720) | ~£100 — an 85–90% collapse in under 4 months |

| Key Architect | Robert Harley (founder, 1711); John Blunt (chief director, 1720 scheme) |

| Most Famous Victim | Isaac Newton — estimated loss of £20,000 |

| Actual Trading Revenue | Near zero. Spain allowed one ship per year. The monopoly was almost entirely fictional. |

| Political Fallout | Chancellor of the Exchequer imprisoned in the Tower of London; multiple MPs expelled; directors’ estates seized |

| Legislative Legacy | Bubble Act 1720 — restricted joint-stock companies for 105 years until repeal in 1825 |

| Who Survived It Well | Robert Walpole — opposed the scheme throughout; managed the aftermath; became Britain’s first Prime Minister |

| M·M·M Lesson | Mind — FOMO destroyed the greatest analytical mind alive. Money — leverage turned a correction into a catastrophe. |

A Kingdom Drowning in Debt

It is 1711. Britain has just emerged from ten years of ruinously expensive war and the financial bill has been devastating. The national debt stood at approximately £10 million. The government was borrowing at punishing interest rates simply to keep functioning.

Robert Harley, the Earl of Oxford, devised an audacious solution: convert that national debt into equity. Creditors would be offered shares in a new company — the South Sea Company — which would receive a monopoly on all British trade with South America and the Pacific in exchange.

There was one problem nobody wanted to address. Britain was still at war with Spain. Spain controlled South America. The monopoly was almost entirely theoretical. The South Sea Company’s actual revenues were almost nothing. But the directors understood that it didn’t matter — as long as the story was maintained, the share price could be managed. And a rising share price was the product they were actually selling.

In 1720, watching John Law’s Mississippi Company drive French share prices into the stratosphere, the South Sea directors lobbied Parliament to let them absorb the entire British national debt — now over £30 million. Parliament approved it in April 1720. What happened next was a masterclass in how a society loses its collective mind.

Exchange Alley: The Anatomy of a Mania

The price in January 1720: £128. By May: £550. By June: £890. By the first week of August — the absolute peak — over £1,000 per share. Eight hundred percent in eight months.

The coffee houses of Exchange Alley were packed beyond capacity. The composer George Frideric Handel invested. Members of the royal household held shares. Even Jonathan Swift, who was writing biting satire about this exact collective delusion, reportedly had money in the market.

The mania spawned hundreds of fraudulent new companies. One raised subscription money for “an undertaking of great advantage, but nobody to know what it is.” Reportedly fully subscribed within hours. The promoter collected his deposits and vanished.

Newton’s Fatal Return

Newton had invested early and sold early — at £350 per share, banking a profit of around £7,000. The disciplined exit. The rational decision. Then the price went to £400. Then £500. Then £600. He watched. Week after week, his friends grew richer.

He bought back in near the top. An estimated £20,000. Everything he had. He didn’t lose because he was stupid. He lost because he was watching. FOMO does not discriminate by IQ.

The Collapse

The South Sea Company had been lending money to shareholders — using their own shares as collateral — so they could buy more shares. The moment prices stopped rising, it became a machine designed to accelerate its own collapse.

By end of August: £800. Margin calls arrived. By mid-September: £400. By end of September: £150. By December: below £100. From over £1,000 to under £100 in four months. Ordinary investors received nothing. No bailout, no rescue. The Chancellor of the Exchequer was imprisoned in the Tower of London. Robert Walpole — who had opposed the scheme throughout — managed the reconstruction and became Britain’s effective first Prime Minister.

What This Means for You as a Trader

🧠 MIND — The Newton Problem

Intelligence does not protect against FOMO. Newton had already made a profitable trade and walked away correctly. He re-entered because watching others profit became psychologically unbearable — not because his analysis changed. The protection isn’t being smarter. It’s having a pre-committed rule, written before the emotion arrives, that defines exactly when you will and won’t enter a position.

📊 METHOD — Story vs. Valuation

South Sea shares hit £1,000 based on revenues that were essentially zero. Nobody asked what the earnings per share were — because there were none. When your investment thesis exists only as narrative rather than numbers, you are speculating. That requires a defined entry, a defined exit, and a position size you can afford to lose entirely.

💰 MONEY — The Leverage Cascade

The South Sea Company’s practice of lending against shares as collateral created a self-reinforcing crash. Falling prices destroyed collateral, forced selling, which dropped prices further. This same structure appears in 1929 margin lending, 2008 mortgage CDOs, 2022 crypto borrowing. Leverage amplifies both directions with equal force. The upside makes people forget this. The downside reminds them, all at once.

Frequently Asked Questions

What did the South Sea Company actually trade?

Almost nothing. The company held a monopoly on British trade with Spanish-controlled South America under the Asiento agreement. In practice, Spain permitted only one British trading vessel per year, and even those voyages were barely profitable. The share price was built entirely on the promise of future wealth that never materialised.

Did Isaac Newton really lose £20,000?

The £20,000 figure is the most widely cited historical estimate. What is confirmed is that Newton made an initial profitable investment, sold early, then re-entered near the peak and suffered substantial losses. His famous quote about heavenly bodies and human madness is attributed to this period. The emotional truth — a supremely rational mind defeated by FOMO — is consistent across all historical accounts.

What was the Bubble Act?

The Bubble Act of June 1720 was passed at the request of South Sea directors who wanted to suppress competing speculative ventures draining money from their own stock. It required parliamentary authorisation for joint-stock companies and remained law for over a century until repeal in 1825. Many historians argue it significantly restricted British corporate innovation during the Industrial Revolution.

Were investors compensated after the crash?

Partially, and inadequately. Directors’ estates were confiscated and distributed — but the recovery was a small fraction of total losses. There was no government bailout. Ordinary investors who speculated and lost bore their losses entirely. The contrast with post-2008 bailouts is instructive: in 1720, moral hazard was resolved entirely by the market itself.

How does this compare to modern speculative manias?

The structural parallels are almost exact. A genuine underlying opportunity used to justify valuations disconnected from real earnings. Leverage amplifying the upside until it amplifies the downside catastrophically. The final wave of buyers — those who watched from the sidelines until the psychological pressure became unbearable — suffering the worst outcomes. The mechanism has not changed in three centuries.

What is the single most important lesson for a modern trader?

The Newton problem. He had already made the right decision — sold profitably, walked away. He reversed it not because his analysis changed, but because watching others profit became psychologically intolerable. The defence is a pre-committed, written trading rule that governs your entry criteria regardless of what the market or other investors are doing. Make the rule when you are calm. Follow it when you are not.

Continue the Market Mayhem Series

Next: Iron Horses and Paper Fortunes

The Railway Mania of the 1840s. Real technology. Real transformation. And a fraud so spectacular it brought down the most powerful businessman in Britain.

⚡ Modern Echo · 2026

The South Sea Company traded shares it created in itself, lending money to buyers so they could buy more shares. The loop held until it didn’t. In 2026, Nvidia invests $100B in OpenAI, which buys $1.4T of Nvidia compute, while Oracle promises $300B more. Every revenue line is somebody else’s capex line. Same loop. Bigger zeros.

Read: The Next Market Crash — 5 Scenarios That Could End the Bull Run →

Market Mayhem is a historical education series produced by The Complete Trader’s Edge. All figures are sourced from historical records. Content is for educational purposes only and does not constitute financial or investment advice. Trading involves significant risk of loss.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →

Greatest Companies

How the world's greatest companies were built — and what traders learn from them.

View on Amazon →