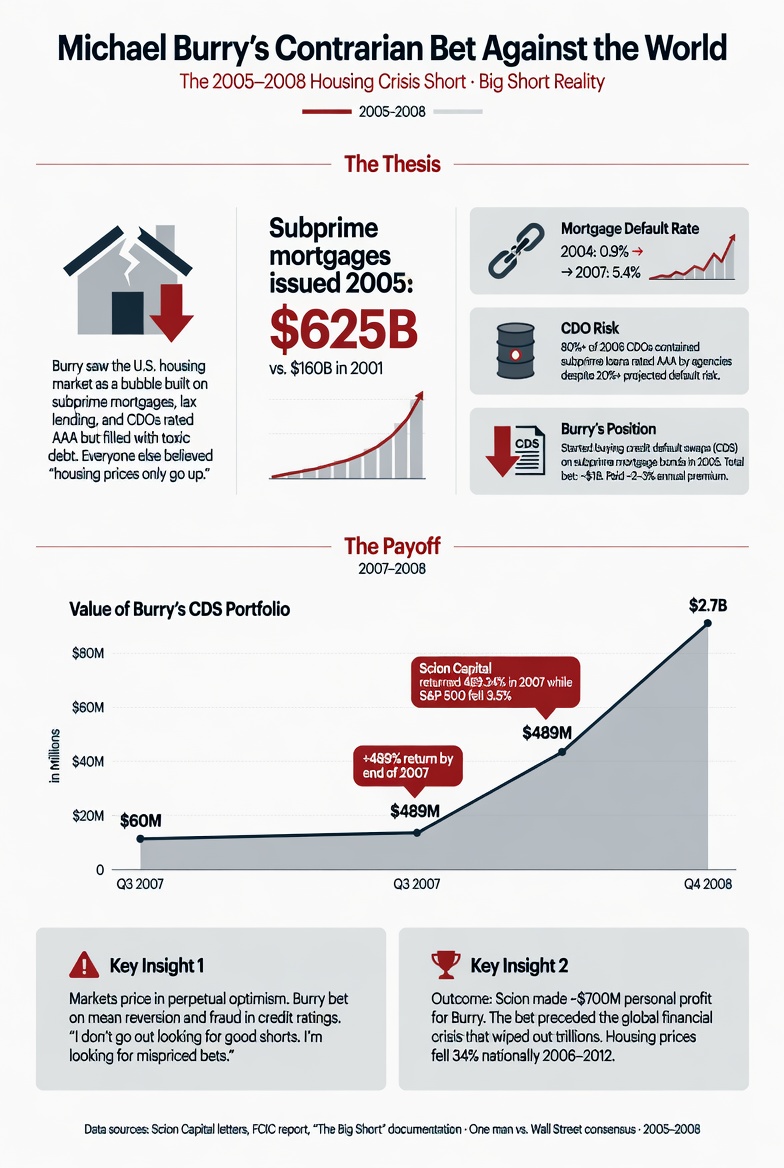

Michael Burry saw the 2008 financial crisis coming years before it arrived. While the entire financial establishment — banks, regulators, rating agencies, and the mainstream media — insisted that American housing was safe, Burry quietly built one of the most asymmetric trades in market history. His fund, Scion Capital, returned 489% between 2000 and 2008. His personal profit from the subprime short alone was approximately $100 million.

But Burry’s story is not primarily about a single trade. It is about what happens when a trader combines deep independent research, extraordinary conviction, and the psychological endurance to hold a position while the entire world tells him he is wrong. That combination of qualities — and the pain it requires — contains lessons that apply directly to every trader reading this.

The Doctor Who Read Footnotes

Michael Burry’s path to finance was unconventional. He trained as a physician at Vanderbilt University School of Medicine and completed a residency in neurology at Stanford. He lost his left eye to retinoblastoma as a toddler and grew up with a prosthetic eye, a condition he has said contributed to a sense of being an outsider — someone who learned to observe the world differently from everyone else.

While completing his medical residency — working eighteen-hour shifts — Burry ran an investment blog in his spare time. His analysis was so sharp that it attracted attention from professional investors. Joel Greenblatt of Gotham Capital offered to seed a fund, and in 2000, Burry left medicine entirely to found Scion Capital.

His early performance was exceptional. While the dot-com bubble devastated most portfolios, Burry’s deep-value approach generated 55% in his first full year while the S&P 500 fell. He did it by reading what nobody else bothered to read: SEC filings, footnotes, credit agreements, and the fine print that companies used to hide unflattering information.

This habit of reading primary sources — not analyst reports, not headlines, not market commentary — would define his entire career. And it is the habit that led him to the trade of the century.

The Big Short: Seeing What Nobody Wanted to See

Starting in 2003, Burry began studying the American mortgage market. Not the headlines about rising home prices or the cheerful assessments from Greenspan’s Federal Reserve. He read the actual mortgage prospectuses — the legal documents describing the loans being bundled into mortgage-backed securities.

What he found was alarming. A growing percentage of mortgages were being issued to borrowers with no income verification, no down payments, and adjustable rates that would reset dramatically higher after two years. These were loans that could only be repaid if house prices continued to rise indefinitely. The entire system was a bet that real estate would never decline nationally.

Burry recognised this as a mathematical certainty waiting to express itself. When adjustable-rate mortgages reset in 2007 and 2008, default rates would spike. The mortgage-backed securities built on these loans would collapse. And the financial institutions holding trillions of dollars of these securities — most without adequate reserves — would face catastrophic losses.

He began purchasing credit default swaps against subprime mortgage bonds. A credit default swap is essentially insurance: Burry paid a premium and would collect if the underlying bonds defaulted. The cost of this insurance was extraordinarily cheap because virtually nobody believed the bonds would fail.

By 2005, he had built a massive short position against subprime — and then he waited.

The Psychological Cost of Being Early

This is the part of Burry’s story that matters most for developing traders, and it is the part that the film The Big Short only partially captures.

Being right early in markets is functionally identical to being wrong. Burry’s credit default swaps cost money every month in premiums. As 2005 turned into 2006 and house prices continued to rise, his investors saw only bleeding capital and an apparently delusional fund manager. They demanded their money back. Some threatened lawsuits. His own partners questioned his sanity.

Burry’s response was to impose a gate — a contractual restriction preventing investors from withdrawing capital. This was legal but deeply unpopular. It made him the villain in his own story. Investors who had entrusted him with their money were told they could not leave, while the fund’s value continued to decline on paper.

The psychological pressure was immense. Burry later described this period as one of the most painful experiences of his life. He was isolated, attacked by the people who should have trusted him, and facing the possibility that his analysis — however correct in theory — might be proven right too late to save his fund.

Then 2007 arrived. Mortgage defaults began exactly as he had predicted. The securities he was betting against started to collapse. By the time the full crisis hit in 2008, Burry’s position had generated enormous profits. Scion Capital returned 489% to its investors from inception. Burry personally made roughly $100 million.

Most of his investors never thanked him.

What Traders Can Learn from Michael Burry

Do Your Own Research — Really Do It

Burry did not arrive at his thesis by reading Goldman Sachs research reports or watching financial television. He read the primary documents. He built his own spreadsheets. He calculated the default probabilities himself. And because he did the work from raw data, he had conviction that no amount of social pressure could shake.

For every trader, the principle is the same: the quality of your conviction depends entirely on the quality of your analysis. If your trade idea came from someone else’s tweet, you will abandon it at the first drawdown. If it came from your own deep work — your own backtesting, your own chart analysis, your own data — you can hold through the noise because you understand why the trade works.

Being Early Is the Cost of Being Right

Burry was early by nearly two years. During those two years, his position showed only losses. This is the reality of many excellent trades: the market can remain irrational longer than your patience or your capital can survive.

The practical lesson: size your positions so that being early does not destroy you. Burry’s credit default swaps had a defined cost — the premiums. He knew exactly what his maximum loss was and could endure it. For discretionary traders, this means using stop losses that give the trade enough room to develop while limiting the damage if the thesis takes time to play out.

Contrarian Conviction Requires Emotional Endurance

The hardest part of Burry’s trade was not the analysis. It was sitting in his office, losing money month after month, while his investors called him a fraud and his colleagues thought he had lost his mind. That requires a specific psychological makeup — a tolerance for isolation and social disapproval that most people simply do not possess.

| Principle | What It Means | Trading Application |

|---|---|---|

| Deep value research | Read primary sources that nobody else reads | Study individual loan documents, company filings, and raw data. Surface-level analysis produces surface-level results. |

| Contrarian conviction | Be willing to bet against the entire market | The best entries feel wrong. If everyone agrees with your trade, the move may already be priced in. |

| Early and patient | The thesis can be right long before the market agrees | Being early is expensive. Budget for it. Keep position sizes manageable during the waiting phase. |

| Defined risk structure | Use instruments with capped downside and uncapped upside | Options strategies, tight stop losses, and asymmetric R:R structures limit what you can lose while preserving what you can gain. |

The fear of being wrong is powerful. But the fear of being right while everyone else disagrees is often even more debilitating. Burry’s story teaches that genuine conviction — the kind built on deep personal research — is the only armour against this pressure.

Asymmetry Is Everything

The credit default swap trade was brilliant not because Burry predicted a crash, but because the risk-reward was absurdly asymmetric. If he was wrong, he lost the premiums — a known, limited amount. If he was right, he stood to make multiples of his investment. This asymmetry is what made the trade worth the pain of being early.

Every trade you take should be evaluated through this lens. What do I lose if I’m wrong? What do I gain if I’m right? Is the ratio worth the risk? This is risk-to-reward thinking at its most fundamental — and Burry demonstrated it at the highest possible stakes.

Post-2008: The Contrarian Continues

Burry closed Scion Capital after the crisis, burned out by the psychological toll. But he returned to investing in 2013 with Scion Asset Management. His subsequent track record has been characteristically contrarian. He made early investments in water rights as a long-term commodity play. He bet against Tesla. He bought GameStop before it became a meme stock phenomenon. He shorted the market in 2023 and took positions against AI-driven tech valuations.

Not every post-2008 call has been perfectly timed. His bearish positions have sometimes been early — the same challenge he faced with subprime. But the pattern is consistent: deep research, independent thinking, willingness to be alone, and the patience to wait for the market to recognise what the data already shows.

Burry is also notable for his disclosure that he has been diagnosed with Asperger’s syndrome (now part of the autism spectrum). He has credited this with his ability to focus intensely on data for extended periods and his relative indifference to social consensus — qualities that, in the context of financial markets, proved extraordinarily valuable.

Burry and the Mind · Method · Money Framework

Mind: Burry’s greatest asset is his psychological independence. He is not swayed by consensus, popularity, or social pressure. He derives his conviction from primary research, which gives him the mental fortitude to hold positions that the rest of the world considers insane. For developing traders, the lesson is that your conviction must be earned through your own work, not borrowed from others.

Method: His method is deep fundamental analysis — reading the documents that nobody else reads, building models from raw data, and identifying asymmetric opportunities where the market has mispriced risk. The discretionary trader’s equivalent is thorough strategy development based on personal backtesting and rigorous trade selection criteria.

Money: Burry’s position sizing on the subprime trade was aggressive but defined. He knew his maximum loss (the premiums) and sized accordingly. He also endured a significant drawdown period — which means his capital management allowed for the possibility of being early. Managing drawdowns while maintaining conviction is perhaps the hardest money management challenge in trading.

The Enduring Lesson

Michael Burry’s legacy is not that he predicted 2008. Plenty of people saw the warning signs. His legacy is that he did the work, built the position, and then survived the psychological and financial cost of being right before the rest of the world was ready to agree with him.

That combination — deep research, asymmetric sizing, and the endurance to hold — is available to every trader. The question is whether you are willing to pay the price it demands.

Key Takeaways from Michael Burry

🔍 Read primary sources. Conviction built on your own research survives pressure that borrowed opinions cannot.

⏳ Being early is the cost of being right. Size your positions so that timing errors don’t destroy you before your thesis plays out.

⚖️ Seek asymmetric trades: defined downside, outsized upside. The risk-reward ratio is more important than the prediction.

🧠 Genuine contrarian thinking requires psychological independence. If your conviction depends on others agreeing with you, it is not conviction.

Explore the Full Legendary Traders Series

Learn from history’s greatest market minds.

George Soros ·

Paul Tudor Jones ·

Jesse Livermore ·

Druckenmiller ·

John Paulson