One of the most liberating realisations in trading is that you do not need to be right most of the time to make money. A trader with a 40% win rate can be consistently profitable. A trader with a 70% win rate can steadily lose money. The difference is the risk-to-reward ratio: the relationship between how much you risk on each trade and how much you stand to gain.

Understanding this relationship transforms how you evaluate setups, manage trades, and define what a “good trade” actually means. It shifts the conversation from “Was I right?” to “Did the maths work in my favour?” This article gives you the full framework for thinking in R-multiples and using risk-to-reward as your primary trade filter.

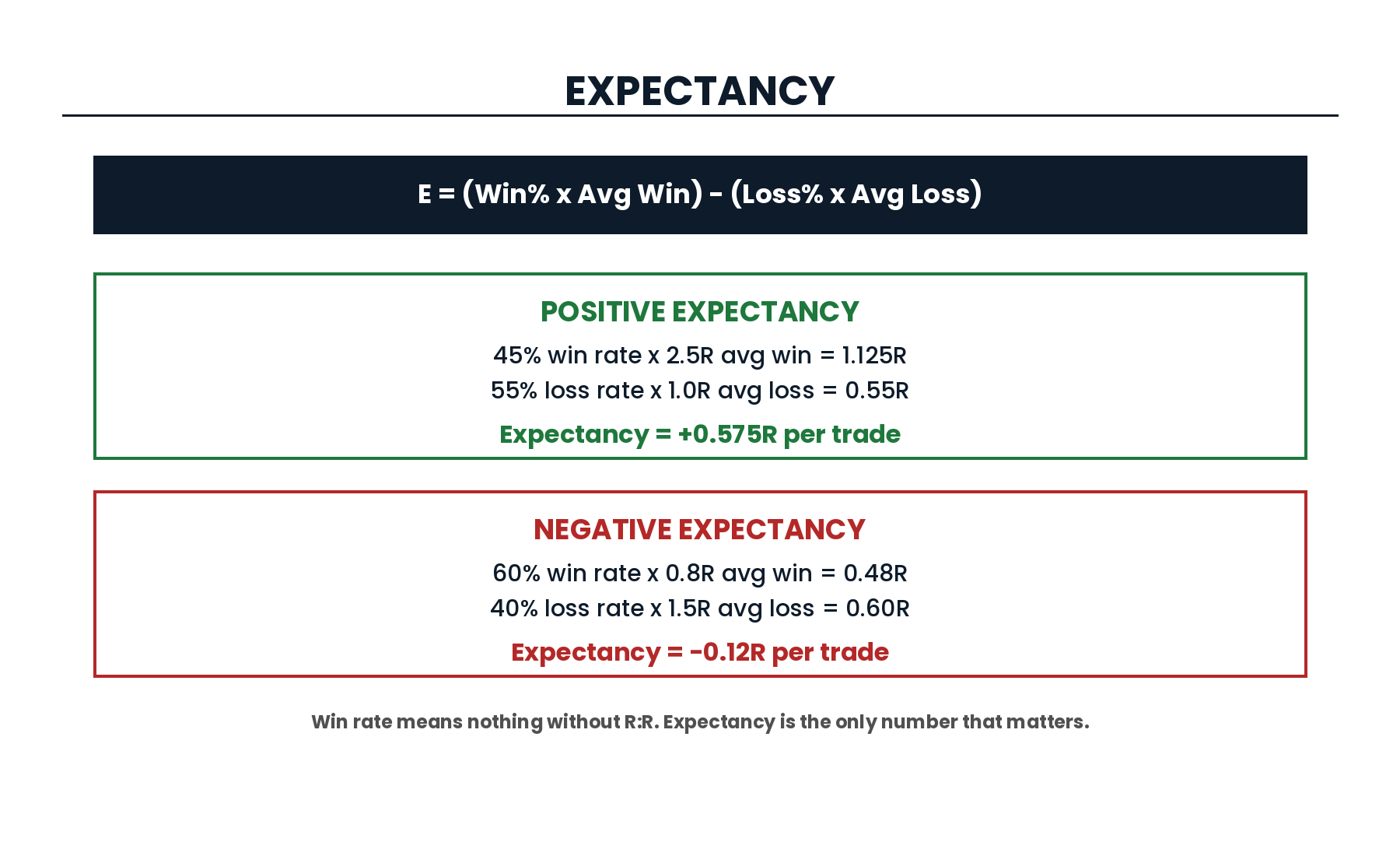

The Mathematics: Why Win Rate Is Only Half the Equation

Consider two traders with very different approaches:

Trader A wins 70% of trades but targets only 1:1 reward-to-risk (making $100 when right, losing $100 when wrong). Over 100 trades: 70 wins x $100 = $7,000 gain. 30 losses x $100 = $3,000 loss. Net: +$4,000.

Trader B wins 40% of trades but targets 2.5:1 reward-to-risk (making $250 when right, losing $100 when wrong). Over 100 trades: 40 wins x $250 = $10,000 gain. 60 losses x $100 = $6,000 loss. Net: +$4,000.

Same profitability from vastly different win rates. Trader B loses more often but makes more when winning. Trader A wins more often but makes less per win. The mathematics of expectancy rewards patience for larger moves as much as it rewards accuracy.

The Breakeven Win Rate Table

This table shows the minimum win rate you need to break even at different risk-to-reward ratios (excluding transaction costs). Any win rate above the breakeven level produces profit.

| Risk-to-Reward Ratio | Breakeven Win Rate | Comfortable Win Rate | Verdict |

|---|---|---|---|

| 1:0.5 (risk more than reward) | 67% | 75%+ | Avoid. Requires very high accuracy. |

| 1:1 | 50% | 55%+ | Marginal. Tight margin for error. |

| 1:2 (professional standard) | 33% | 40%+ | Excellent. Large margin for being wrong. |

| 1:3 | 25% | 30%+ | Highly forgiving. Can be wrong 70% of the time. |

| 1:5 | 17% | 22%+ | Very forgiving, but harder to find setups that deliver 5R. |

The key insight: at 1:2 R:R, you only need to win 34% of trades to be profitable. This means you can be wrong on two out of every three trades and still make money. When you internalise this, the pressure to be “right” on every trade disappears, and with it goes much of the fear and analysis paralysis that plagues retail traders.

Thinking in R-Multiples

Professional traders do not think in dollars. They think in R. 1R is your risk on a single trade. If you risk $100 per trade, 1R = $100. A 2R winner is a $200 gain. A 3R winner is $300. A full stop loss is -1R.

Measuring performance in R-multiples normalises results across different account sizes and instruments. A trader making 15R per month on a $10,000 account has exactly the same skill level as a trader making 15R on a $500,000 account. The dollar amounts are different. The performance is identical.

Track your weekly and monthly R. After 50+ trades, your average R per trade is your expectancy. If your average R per trade is +0.25R, you expect to make 0.25 units of risk on every trade you take. Multiply that by your trade frequency and you have your expected monthly return.

How Traders Destroy Their R:R in Practice

Understanding R:R in theory is easy. Maintaining it in practice is where most traders fail. The three most common ways traders degrade their reward-to-risk:

Exiting early out of fear. Price is 70% of the way to your target. You feel the urge to take profit “before it comes back.” You close at 1.4R instead of the planned 2R. Over 100 trades, this systematic reduction cuts your total profit by 30% or more. The fear of giving back open profits is one of the most expensive emotions in trading.

Moving targets further away. The opposite problem: greed causes the trader to extend their target from 2R to 3R mid-trade because “it has more to give.” The result is often that the market reverses before reaching the extended target, and a clean 2R win becomes a breakeven or a loss.

Widening stops after entry. When price moves against the trader, they move the stop further away to “give it more room.” This increases the R (risk) side of the ratio, degrading the setup from 1:2 to 1:1 or worse. The trade now needs a much higher win rate to be profitable, and the trader has accepted more risk than planned.

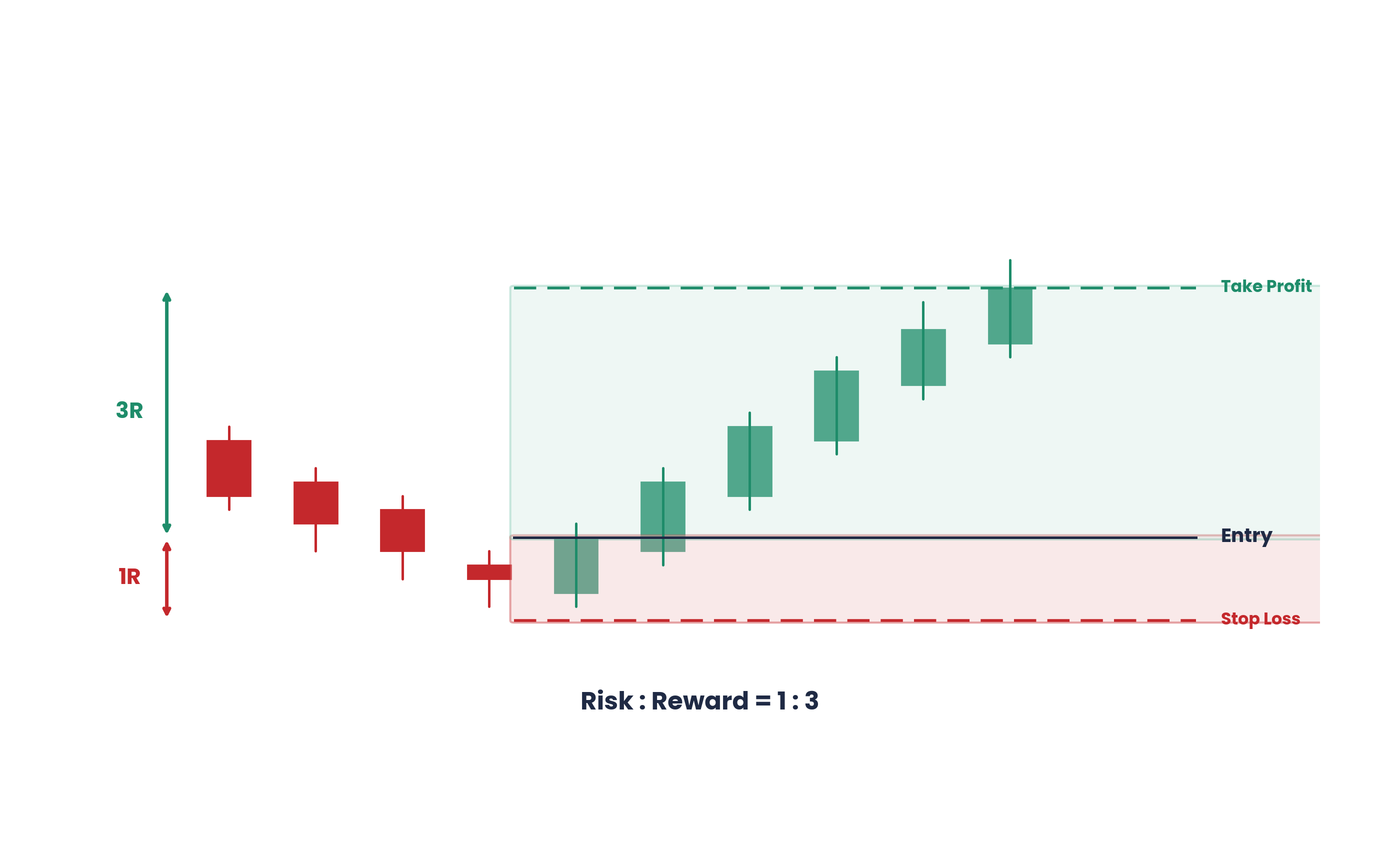

Using R:R as a Trade Filter

Before entering any trade, calculate the R:R based on your planned entry, stop, and target. If the stop loss is 20 pips and the target is 40 pips, the R:R is 1:2. If the stop is 20 pips and the target is 15 pips, the R:R is 1:0.75. The second trade is a bad trade regardless of how perfect the setup looks, because the mathematics are working against you.

Make it a hard rule: no trades below 1:2 R:R. This single filter eliminates a massive number of mediocre setups and keeps you focused on trades where the maths are in your favour. Some traders set their minimum at 1:1.5 and look for 1:3 as the ideal. The exact number is less important than having a non-negotiable floor.

Key Lessons

- A high win rate is not required for profitability. Risk-to-reward ratio is equally important.

- At 1:2 R:R, you are profitable winning only 34% of trades. This transforms how you think about being “wrong.”

- Think in R-multiples, not dollars. 1R = your risk per trade. Track average R per trade as your primary performance metric.

- The three ways traders destroy R:R: exiting early (fear), extending targets (greed), and widening stops (loss aversion).

- Use R:R as a pre-entry filter. No trades below 1:2 minimum.

Frequently Asked Questions

Is a higher risk-to-reward ratio always better?

Not necessarily. Higher R:R targets (1:3, 1:5) mean fewer winning trades because price has to travel further to reach the target. A 1:5 setup with a 15% win rate produces the same expectancy as a 1:2 setup with a 40% win rate. The choice depends on your psychology and trading style. Traders who struggle with losing streaks may prefer higher win rates (and accept lower R:R). Traders who are comfortable being wrong frequently can target higher R:R and enjoy fewer but larger wins.

How do I find high R:R setups consistently?

High R:R setups typically occur at key structural levels where the stop can be tight (close to invalidation) and the target is far (next major level). Order Block entries with stops below the OB and targets at the next liquidity pool naturally produce 1:2 to 1:4 ratios. Golden Pocket entries (0.618-0.702 Fibonacci) with stops below the 0.786 also offer excellent R:R because the stop is structurally tight.

Should I use fixed targets or trailing stops?

Both have merit. Fixed targets are simpler and guarantee you capture the planned R:R when price reaches the target. Trailing stops potentially capture larger moves (3R, 5R) but risk giving back unrealised profit when price reverses. Many traders use a hybrid: take partial profit at the fixed target (e.g., close 50% at 2R) and trail the remaining 50% with a structure-based stop. This locks in guaranteed profit while allowing the trade to run.

My backtesting shows good R:R but live results are worse. Why?

The most common cause is slippage between planned exits and actual exits. In backtesting, you record the target price as the exit. In live trading, fear causes early exits, cutting winners at 1.5R instead of 2R. Spread and slippage also reduce the effective R:R. The solution is automation where possible (set limit orders at your target) and rigorous journal tracking of planned vs actual exit prices so you can measure the gap and work to close it.

How does risk-to-reward connect to the Mind, Method, Money framework?

R:R sits at the intersection of Method and Money. It is a Method concept because your setup structure determines the available R:R (entry, stop, and target locations). It is a Money concept because it determines your expectancy and long-term profitability. And it connects to Mind because the psychological ability to hold a trade to its target without interfering is ultimately a Mind pillar skill.

Continue Reading

▶ Stop Losses: Why They Are Non-Negotiable

▶ Risk of Ruin: The Mathematics Every Trader Must Understand

From The Book

This article covers concepts from Chapter 57 of The Complete Trader’s Edge.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →