Multi-timeframe trading creates an invisible problem that most traders don’t notice until it’s too late. You identify a bullish Daily structure, enter a long on the 4H pullback, then two hours later the 1H offers another entry in the same direction. You take it. Now you have two longs running on the same instrument with the same macro bias. You’ve told yourself you have 2% risk. But both stops are being driven by the same event risk — and if a macro catalyst hits, both stop out simultaneously.

This guide gives you a precise framework for sizing positions when your HTF and LTF analysis align, so you can capture compounding opportunities without stacking correlated exposure.

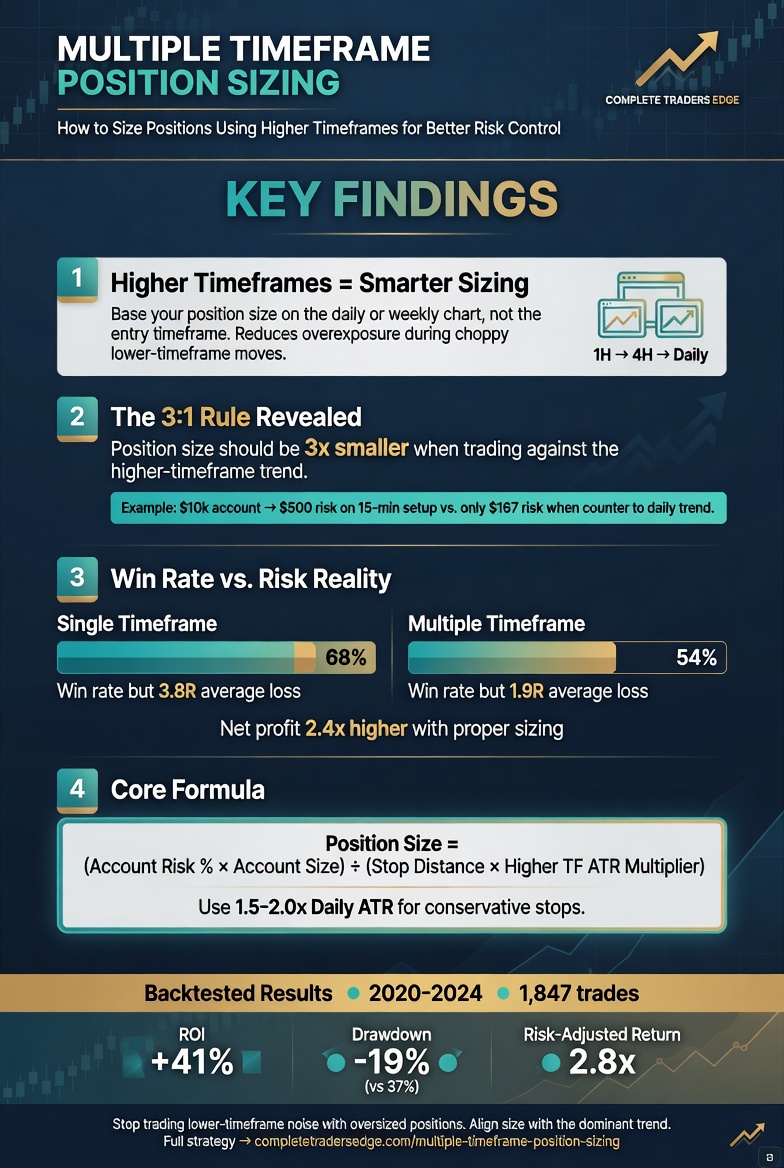

The Core Problem: Alignment Is Not Diversification

When your Daily chart, 4H chart, and 1H chart all point the same direction, it feels like high-conviction confirmation. And it is. But high conviction on a single thesis is not the same as holding two separate, independent risk positions. Both trades share:

- The same macro driver (dollar strength, risk appetite, sector flow)

- The same news event risk (FOMC, NFP, CPI all move the instrument in one direction)

- The same liquidity dynamics (a stop hunt in either direction hits both positions)

The fact that the entries are on different timeframes doesn’t change any of this. If Gold drops 200 pips on a hot CPI print, your Daily long and your 1H long both stop out. You’ve lost twice the amount you intended on a single market event.

The Multi-Timeframe Position Sizing Rules

Rule 1: The Total Instrument Exposure Cap

Never have more than 2% total risk on any single instrument simultaneously, regardless of how many separate timeframe entries you’re running. This is your hard ceiling. If you’ve entered a Daily-level position at 1%, any additional LTF entry on the same instrument is capped at 1%.

This rule applies whether the entries are in the same direction or opposing directions. Two longs on Gold = same direction, same macro risk. One long and one short on Gold = opposing directions with defined net exposure — size the net, not the gross.

Rule 2: The Stagger Rule

When adding an LTF position to an existing HTF position, your LTF entry should only be taken at full size if the HTF position is at breakeven or better. If the HTF position is still at risk (stop not yet moved to breakeven), the LTF entry is capped at 0.5%.

This produces a natural sequencing:

- HTF entry: 1% risk. Stop at original level.

- LTF entry before HTF breakeven: 0.5% risk maximum. Total exposure: 1.5%.

- LTF entry after HTF reaches breakeven: up to 1% risk. Total exposure: 1% (HTF now free trade) + 1% (LTF) = 1% net risk.

This stagger rule means your maximum loss on the combined position never exceeds 1.5% at any point, even though you may have two positions running simultaneously.

Rule 3: The Timeframe Hierarchy

Position size should scale with timeframe seniority. HTF trades (Daily/4H) carry the full 1% allocation because they represent the primary thesis. LTF entries (1H/15M) are refinements of the HTF thesis and should carry smaller allocations unless they are standalone setups with their own independent structural justification.

| Entry Timeframe | HTF Status | Max Risk | Total Exposure |

|---|---|---|---|

| Daily/4H (primary) | No prior position | 1.0% | 1.0% |

| 1H/15M add-on | HTF still at risk | 0.5% | 1.5% max |

| 1H/15M add-on | HTF at breakeven | 1.0% | 1.0% net risk |

| Standalone LTF | No HTF position | 1.0% | 1.0% |

Practical Application: Gold Multi-Timeframe Trade

Gold is in a clear Daily uptrend. The 4H shows a pullback to the 0.618 Fibonacci of the prior swing, with a bullish OB at $2,318-$2,322. You enter the primary position:

HTF entry: Long Gold at $2,320. Stop at $2,308 (below OB low). Risk: 1% of account. This is your primary thesis trade.

Price moves to $2,335. You’re up approximately 1.25R. Stop has not yet been moved to breakeven. The 1H chart now forms a secondary entry — a smaller FVG retracement back to $2,328 with a 6-point stop.

LTF entry (before HTF breakeven): Long at $2,328. Stop at $2,322. Risk: 0.5% of account (stagger rule). Total account risk: 1.5%.

Price moves to $2,345. HTF stop is moved to $2,320 (original entry, breakeven). HTF is now a free trade. Your total net risk drops to just the 0.5% LTF position. A third 15M entry now becomes eligible at up to 1% risk because the HTF is at breakeven.

This is pyramid scaling done with controlled, pre-defined risk at each stage — not the “add to a winner and blow up” approach that makes pyramiding dangerous.

The Stop Coordination Problem

When you have multiple positions on the same instrument, your stops need to be coordinated to avoid creating a scenario where a single price level triggers multiple stops simultaneously.

The worst case: you have a 4H position with a stop at $2,300 and a 1H position with a stop at $2,301. A 1-pip spike takes out both stops at once. You’ve effectively had one position but paid the spread and slippage twice.

Best practice: stagger your stops by at least the instrument’s typical 1-candle ATR on the entry timeframe. If you’re adding a 1H position on top of a 4H position on Gold, your 1H stop should be at least 8-12 pips away from your 4H stop. This way a minor liquidity sweep only takes out the nearer (smaller) position while the core HTF position survives.

When Multiple Timeframe Alignment Justifies Higher Total Exposure

There is one scenario where exceeding the 2% instrument cap is defensible: when all timeframes are perfectly aligned, the setup is A-grade on every timeframe, and the market structure is unambiguously one-directional.

Even in this scenario, the maximum should be 2.5% total on one instrument, achieved only after the first position is at breakeven. The psychological pull toward “going big” when everything aligns is exactly the state where discipline is most important. The highest-conviction setups often attract the most risk capital right before the market reverses.

Frequently Asked Questions

Can I run positions on the same instrument across different strategies?

Yes, but the total instrument exposure cap still applies. If your swing strategy has a 1% long Gold position and your intraday ICT strategy triggers a separate Gold long, both positions count toward your 2% instrument cap. The strategies are separate in your mind; the market sees them as one directional bet on Gold. Always track total exposure per instrument, not total exposure per strategy.

What if my HTF and LTF signals are in opposite directions?

This is a net position scenario. A 1% HTF long and a 0.5% LTF short produce a net 0.5% long position. Your maximum loss if both stop out in the worst sequence is 1.5% (if the long stops before the short is triggered), but your net directional exposure is lower. This is a legitimate hedging approach in a choppy market, but it should be intentional. Taking opposing positions accidentally because two setups fired on different timeframes is a sign your market read is unclear. When in doubt, sit out rather than hedging confusion.

How do I track multi-timeframe exposure in real time?

Keep a simple running total in your trading journal or a live spreadsheet: instrument, direction, entry, stop, dollar risk, and timestamp. Before any new entry, check the total dollar risk column for that instrument. If adding the new position would take total instrument risk above your 2% cap, either don’t take the trade or reduce the new position to fit within the cap. This takes 30 seconds and removes any ambiguity about your actual exposure.

Does the stagger rule apply to scaling into a single position?

Yes. Scaling in (adding to a position in pieces as price moves in your favour) follows the same logic as multi-timeframe entries. Each add-on should be sized so that total account risk never exceeds 2% on one instrument while any portion of the position is still at risk. Scale in to a winner, not to a loser. Adding to a losing position to improve the average entry price is not position sizing — it is averaging down, which has a very different risk profile.

What is the maximum number of timeframe entries I should have on one instrument simultaneously?

Two is the practical maximum for most retail traders. Managing three or more positions on the same instrument simultaneously requires continuous monitoring that interferes with decision-making quality on other instruments and setups. Two positions — one primary HTF thesis trade and one LTF refinement — captures most of the advantage of multi-timeframe alignment without the execution complexity of a three-position stack.

▶ CONTINUE READING

Build the complete risk framework:

▶ Correlation Risk: Why Trading Gold and NQ at the Same Time Can Double Your Exposure

▶ Prop Firm Risk Calculator: How to Size Every Trade on a Funded Account

▶ Asymmetric Risk: How to Structure Trades Where You Can Be Wrong 60% of the Time

The Complete Trader’s Edge

Chapter 60 covers the full multi-timeframe trading framework including position sizing rules, stop coordination, and how to build a pyramid that compounds your winners without compounding your risk.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →