Almost every trader knows they should have a “good risk-reward ratio.” Most quote a 1:2 or 1:3 as the goal. Far fewer understand what risk-reward actually means in a probabilistic sense, or why a 1:2 ratio tells you almost nothing about whether a strategy is profitable without knowing the win rate it accompanies.

What Risk-Reward Ratio Actually Means

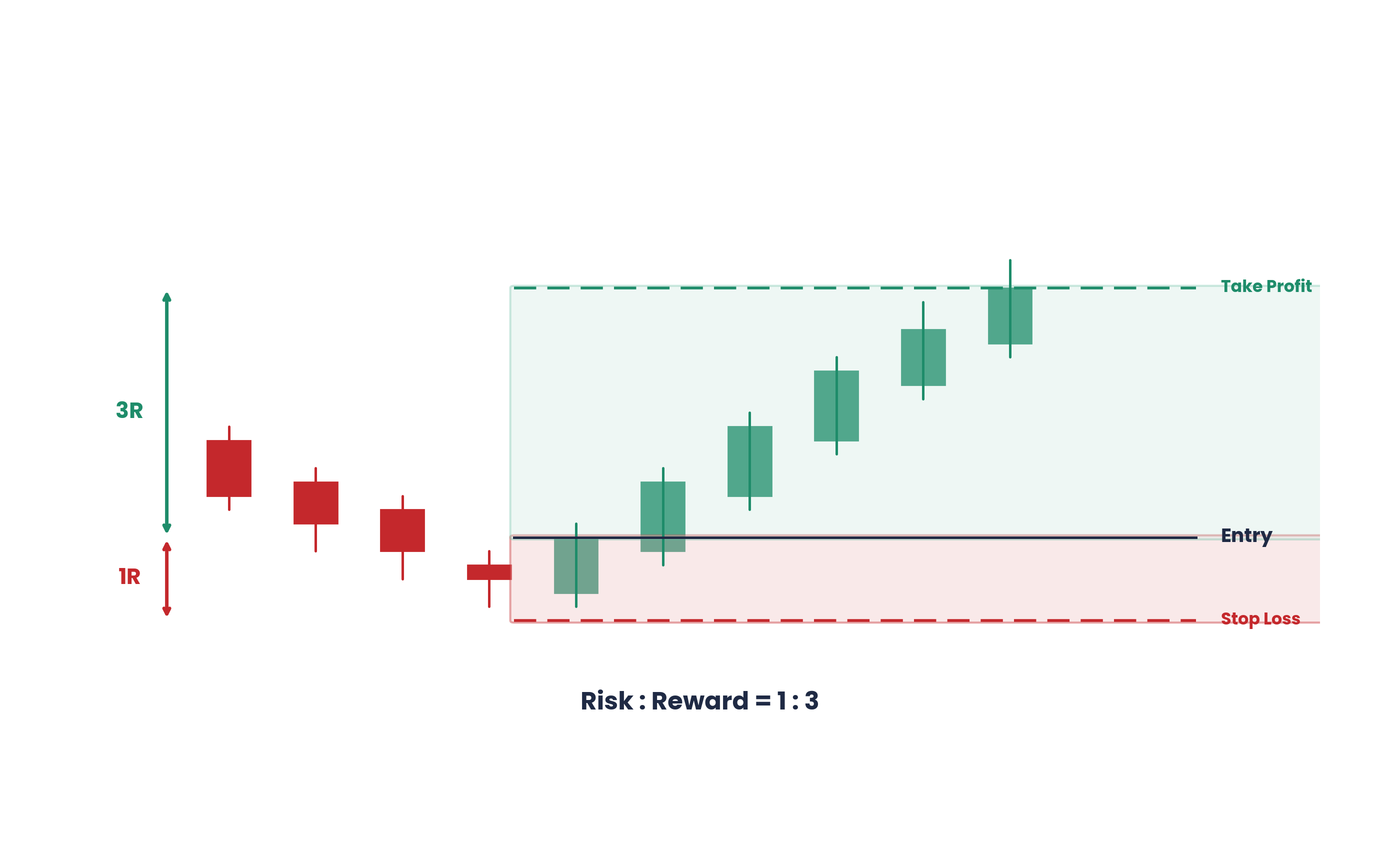

The risk-reward ratio expresses the relationship between your maximum potential loss (risk) and your maximum potential gain (reward) on a single trade. A 1:2 risk-reward ratio means that for every $1 you risk, you stand to make $2 if the trade reaches your target.

Why Risk-Reward Alone Is Meaningless

A 1:3 risk-reward ratio sounds excellent. But if your win rate is 20%, you will still lose money. A 1:1 risk-reward ratio sounds poor. But if your win rate is 60%, you will be consistently profitable. What actually matters is expectancy — the combination of win rate and risk-reward that tells you how much you expect to make per trade on average.

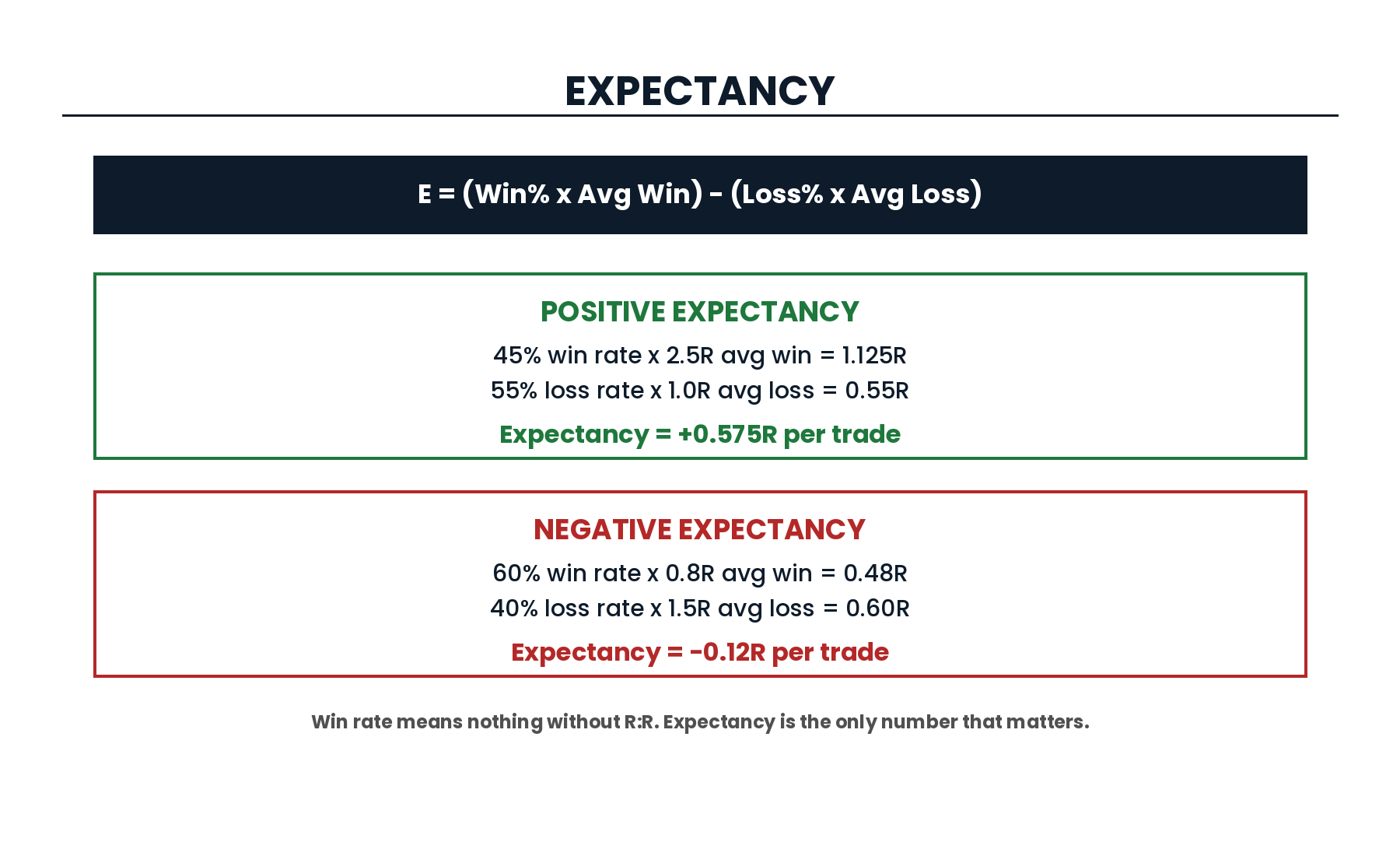

Calculating Trading Expectancy

Expectancy = (Win Rate × Average Win) – (Loss Rate × Average Loss)

Example with a 1:2 risk-reward system at 45% win rate:

- Win rate: 45%, Loss rate: 55%

- Average win: 2R, Average loss: 1R

- Expectancy: (0.45 × 2) – (0.55 × 1) = 0.90 – 0.55 = +0.35R per trade

This system is profitable despite losing more than it wins, because winners are twice the size of losers. A positive expectancy is the mathematical definition of a trading edge.

Setting Realistic Targets

One of the most common mistakes is setting targets that are unrealistically far away to achieve a “good” risk-reward ratio on paper, while placing stops so tight that they are regularly hit by normal market noise. Set your targets at logical price levels — areas of liquidity, opposing structure, or clear resistance — not at arbitrary distances designed to hit a ratio target.

Key Lessons

- Risk-reward ratio in isolation is meaningless — it must be combined with win rate to calculate expectancy.

- Expectancy = (Win Rate × Average Win) – (Loss Rate × Average Loss). Positive expectancy = a real edge.

- A system with a low win rate can be profitable if the risk-reward is high enough — and vice versa.

- Targets should be set at logical price levels, not at arbitrary distances to hit a desired ratio.

→ Related: Risk Management: Complete Framework | Position Sizing Explained

Frequently Asked Questions

What is a good risk-to-reward ratio?

A minimum of 1:2. At 1:2, you need only a 34% win rate to break even. Most ICT traders target 1:2 to 1:3. Below 1:1, the maths work against you.

Should I always aim for the highest R:R?

Not necessarily. Higher targets mean fewer wins. A 1:5 with 15% win rate equals a 1:2 with 40% win rate in expectancy. Choose what matches your psychology.

How do I calculate R:R before entry?

Distance from entry to stop = risk (1R). Distance from entry to target = reward. Divide reward by risk. 50 pip target / 20 pip stop = 1:2.5.

Why are my live R:R results worse than backtesting?

Early exits from fear. Track planned vs actual exit prices in your journal. The gap is the cost of fear.

Does R:R apply to scalping?

Yes. A scalper risking 5 pips to target 10 pips has 1:2 R:R. The principle is timeframe-agnostic. Maintain 1:1.5 minimum even on the lowest timeframes.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →