The institutional benchmark price — session VWAP, swing anchoring, and mean reversion entries.

If you work at a hedge fund and your portfolio manager tells you to buy ten million dollars of stock, the first question your execution desk asks is not whether the stock will go up. It is whether the average fill price was better or worse than VWAP. If you bought below VWAP, you did a good job. If you bought above VWAP, you overpaid. The stock could go up 20% and your execution would still be considered poor if you paid above VWAP to get in.

| VWAP Application | How Institutions Use It | How Retail Traders Can Apply It |

|---|---|---|

| Session VWAP | Benchmark for evaluating execution quality | Dynamic intraday S/R. Price above VWAP = bullish. Below = bearish. |

| Anchored VWAP (AVWAP) | VWAP anchored to a specific event (earnings, swing low, news) | Anchor to significant swing points to identify where the average institutional position sits. |

| VWAP + standard deviations | Statistical extremes from the mean price | Mean reversion entries at +/-2 SD. Trend continuation entries at VWAP retest. |

| Multi-day VWAP | Longer-term institutional cost basis tracking | Weekly VWAP for swing traders. Monthly VWAP for position context. |

This is why VWAP matters. It is the single most important benchmark price for institutional execution. Banks, hedge funds, and algorithmic trading systems all measure their performance against it. And because institutions care about it, price reacts to it. VWAP is not just an indicator — it is a level that drives actual institutional behaviour.

What VWAP Measures

VWAP stands for Volume Weighted Average Price. It calculates the average price of an instrument over a period, weighted by the volume traded at each price. If 80% of the day’s volume traded at $100 and 20% traded at $105, VWAP would be close to $101 — not $102.50. The volume weighting pulls VWAP toward the prices where the most activity occurred.

Standard session VWAP resets at the start of each trading session. Because VWAP incorporates both price and volume, it reflects the actual average cost basis of everyone who traded during the session. If price is above VWAP, the average buyer is in profit. If price is below VWAP, the average buyer is at a loss.

VWAP as Dynamic Support and Resistance

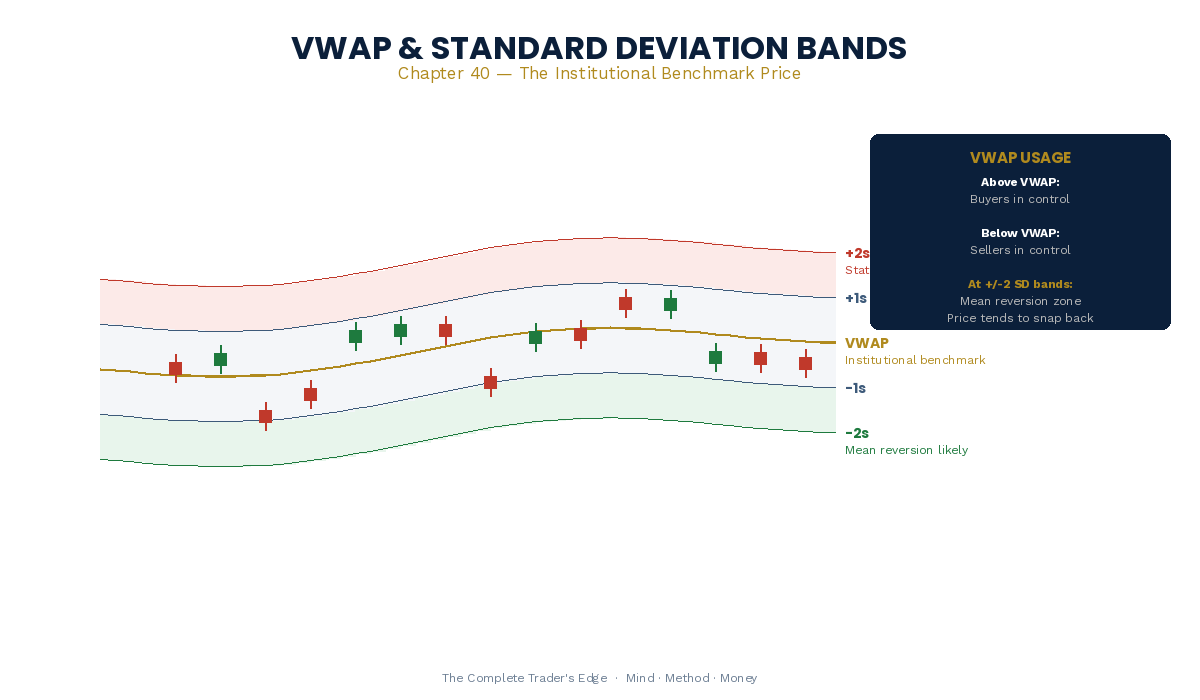

In a trending session, VWAP acts as dynamic support in uptrends and dynamic resistance in downtrends. Pullbacks to VWAP in a trending market offer entries in the direction of the trend. In a ranging session, price oscillates around VWAP — creating mean reversion opportunities: buy below VWAP, sell above VWAP.

The most important VWAP signal is a change in regime. If price spent the first half of the session above VWAP and then breaks below it convincingly, the session bias has shifted. The short-term balance of power has changed.

VWAP Standard Deviation Bands

Most VWAP implementations include standard deviation bands — typically at 1 and 2 standard deviations above and below. The first standard deviation contains roughly 68% of all price action. The second standard deviation contains roughly 95%. When price reaches the 2nd standard deviation, it is statistically extended and more likely to revert toward VWAP.

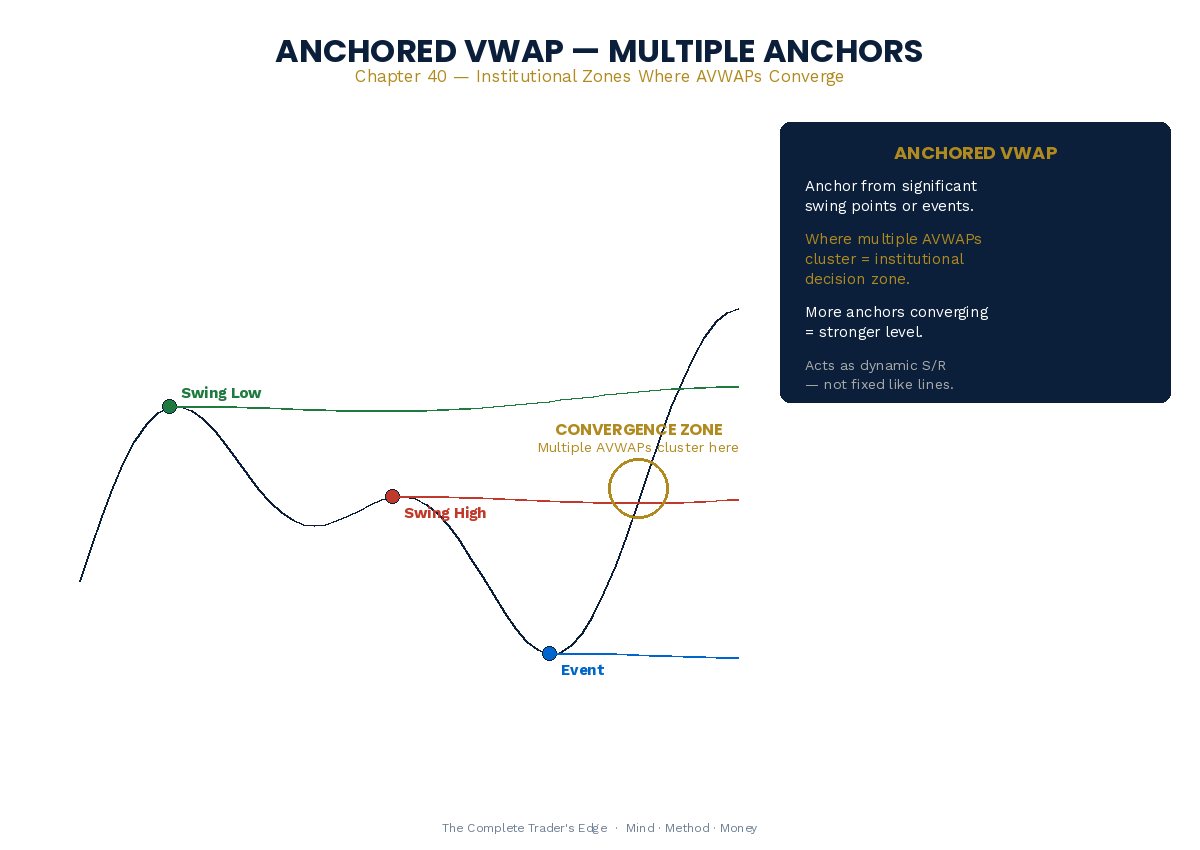

Anchored VWAP

Session VWAP resets every day. Anchored VWAP does not. You choose the starting point — a swing high, a swing low, an earnings date, a news event — and the VWAP calculation runs from that point forward without resetting. This transforms VWAP from an intraday tool into a multi-timeframe tool.

An Anchored VWAP from a major swing low shows you the average cost basis of every buyer since that low. As long as price stays above that level, the trend is healthy. When price breaks below it, the average buyer is now at a loss, creating selling pressure.

Where to Anchor

The most useful anchor points are significant swing highs and lows, the start of a major trend, high-impact news events, the beginning of a quarter, and earnings announcements. The key principle is to anchor from events that changed market behaviour.

Multi-Anchor Analysis

Using two or three Anchored VWAPs simultaneously creates a powerful framework. The zone where these VWAPs converge represents a dense area of average cost basis from multiple perspectives. Price tends to react strongly at these convergence zones.

VWAP and Volume Profile Together

VWAP and Volume Profile are complementary tools. Volume Profile shows you where volume accumulated at static levels. VWAP shows you the dynamic average cost basis that evolves through time. When a Volume Profile VPOC aligns with VWAP or an Anchored VWAP, you have a confluence of the two most institution-watched volumetric levels — a high-probability reaction zone.

📚 Related Articles:

This article is adapted from The Complete Trader’s Edge

70 chapters covering Mind · Method · Money — the most comprehensive trading education framework available.

Frequently Asked Questions

What is VWAP and why do institutions use it?

VWAP (Volume Weighted Average Price) calculates the average price of an instrument weighted by volume throughout the session. Institutions use it as a benchmark: if they buy below VWAP, they got a better-than-average price. For retail traders, VWAP acts as dynamic support and resistance. Price above VWAP suggests bullish sentiment; below suggests bearish.

How do I use VWAP with ICT concepts?

VWAP adds confluence to ICT entries. An Order Block that aligns with VWAP creates a higher-probability zone because you have both institutional structural levels and the institutional benchmark at the same price. Use VWAP as a directional filter: only take longs above VWAP and shorts below VWAP during your Kill Zone.

Does VWAP work on forex or only stocks?

VWAP works on any instrument with volume data. On stocks and futures (ES, NQ, Gold futures), VWAP uses real exchange volume. On forex, VWAP uses tick volume (a proxy), which is less precise but still useful as a directional filter. VWAP is most reliable on instruments with centralised exchange data.

What is anchored VWAP?

Anchored VWAP (AVWAP) is VWAP calculated from a specific reference point: a swing high, swing low, earnings date, or any significant event. This is more flexible than session VWAP because it shows the average price from the event that matters to your analysis. AVWAP from a significant swing low often acts as strong support during the subsequent trend.

Should I use VWAP for entries or exits?

Primarily as a directional filter and confluence factor, not as a standalone entry or exit signal. VWAP tells you whether buyers or sellers are in control on average. Combine it with ICT entries for timing. VWAP says “look for longs.” The Order Block says “enter here.”

From The Book

This article covers concepts from Chapter 37 of The Complete Trader’s Edge.

Frequently Asked Questions

What is VWAP and why do institutions use it?

VWAP (Volume Weighted Average Price) is the average price of an instrument weighted by volume throughout the trading session. Institutions use it as a benchmark: if they buy below VWAP, they got a better price than average. If they sell above VWAP, they sold at a premium. This makes VWAP the most important intraday reference level for institutional order execution.

How do I use VWAP in my trading?

VWAP acts as dynamic intraday support and resistance. When price is above VWAP, the intraday bias is bullish (buyers are in control on average). When below, the bias is bearish. Pullbacks to VWAP in a trending session often provide entry opportunities. VWAP also helps you assess whether your entry price is good relative to the session average.

Does VWAP work for swing trading?

Standard VWAP resets each session, making it primarily a day trading tool. However, Anchored VWAP (AVWAP), which you anchor to a specific event like an earnings release or a market structure break, works across multiple days and is valuable for swing traders. AVWAP from a major swing low shows the average institutional entry price since that event.

How does VWAP compare to moving averages?

Moving averages weight all prices equally. VWAP weights by volume, giving more significance to prices where more trading occurred. This makes VWAP more responsive to genuine institutional activity and less influenced by low-volume noise. For intraday trading, VWAP is superior to moving averages as a directional filter.

Can I combine VWAP with ICT concepts?

Yes, and this combination is powerful. When an Order Block aligns with VWAP during a Kill Zone, you have three layers of confluence: institutional level (OB), volume benchmark (VWAP), and session timing (Kill Zone). These high-confluence zones produce some of the best intraday setups available.

From The Book

This article covers concepts from Chapter 36 of The Complete Trader’s Edge.

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

The Complete Trader's Edge

The full Mind · Method · Money framework. 70 chapters.

View on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →

Market Mayhem

400 years of bubbles, crashes, and the pattern that keeps repeating.

Buy on Amazon →